Written by

Kelsey Syvrud, PhD

Written by

Kelsey Syvrud, PhD

Published on

June 10, 2026

Category

Investment Insights

Kevin Warsh has taken over as Chair of the Federal Reserve (“Fed”) at a particularly sensitive time for markets. Inflation remains a central concern, long-term interest rates are still elevated relative to much of the post-2008 period, and investors are trying to understand whether a new Fed chair means a new policy regime.

The short answer is potentially, but not immediately and not unilaterally.

Warsh brings a distinct set of views to the Fed. He has previously criticized the central bank’s heavy reliance on quantitative easing (“QE”), its large balance sheet, and what he views as an expansion of the Fed’s role beyond its core monetary policy responsibilities. He has also signaled interest in a more restrained communications approach, less dependence on forward guidance, and renewed emphasis on the Fed’s statutory mandate.

For investors, the important question is not simply whether Warsh wants lower short-term rates or a smaller Fed balance sheet. It is whether those goals can be implemented within the institutional structure of the Fed, and what the market implications may be if short-term and long-term rate dynamics move in different directions.

Based on his public comments, confirmation testimony, and recent commentary from Fed watchers, Warsh’s policy framework appears to center on four broad priorities: a narrower interpretation of the Fed’s role, less reliance on extraordinary policy tools, a less scripted communications strategy, and a different way of thinking about inflation.

First, Warsh has argued for a Fed that focuses more narrowly on its core monetary policy mandate. The Fed’s statutory objectives are to promote maximum employment, stable prices, and moderate long-term interest rates. In market shorthand, this is often referred to as the Fed’s “dual mandate” of employment and inflation, but the statute itself also references long-term interest rates. Warsh’s critique is that, in recent years, the Fed has become too willing to comment on or engage with issues that sit adjacent to, but not always directly within, that monetary policy mandate.

This does not mean the Fed would stop caring about financial stability, bank supervision, payment systems, cybersecurity, or liquidity in funding markets. Those are part of the Fed’s broader responsibilities and, in some cases, are central to how monetary policy is implemented. For example, the Fed cannot set policy effectively if short-term funding markets are impaired, if banks are undercapitalized, or if payment systems are unstable. However, Warsh appears more skeptical of the Fed expanding its public role into other areas unless those issues have a clear and direct connection to monetary policy, bank regulation, or financial stability.

For investors, the practical implication is that a Warsh Fed may try to re-establish a cleaner boundary between monetary policy and other policy debates. That could mean fewer public comments from Fed officials on topics outside inflation, labor markets, banking, financial stability, and market functioning. It could also mean a more restrained institutional posture during periods of market stress. In other words, investors may need to distinguish between the Fed acting to preserve market functioning and the Fed acting to support asset prices. Warsh’s prior comments suggest he may be more comfortable allowing markets to absorb discomfort, so long as the financial system itself remains functional.

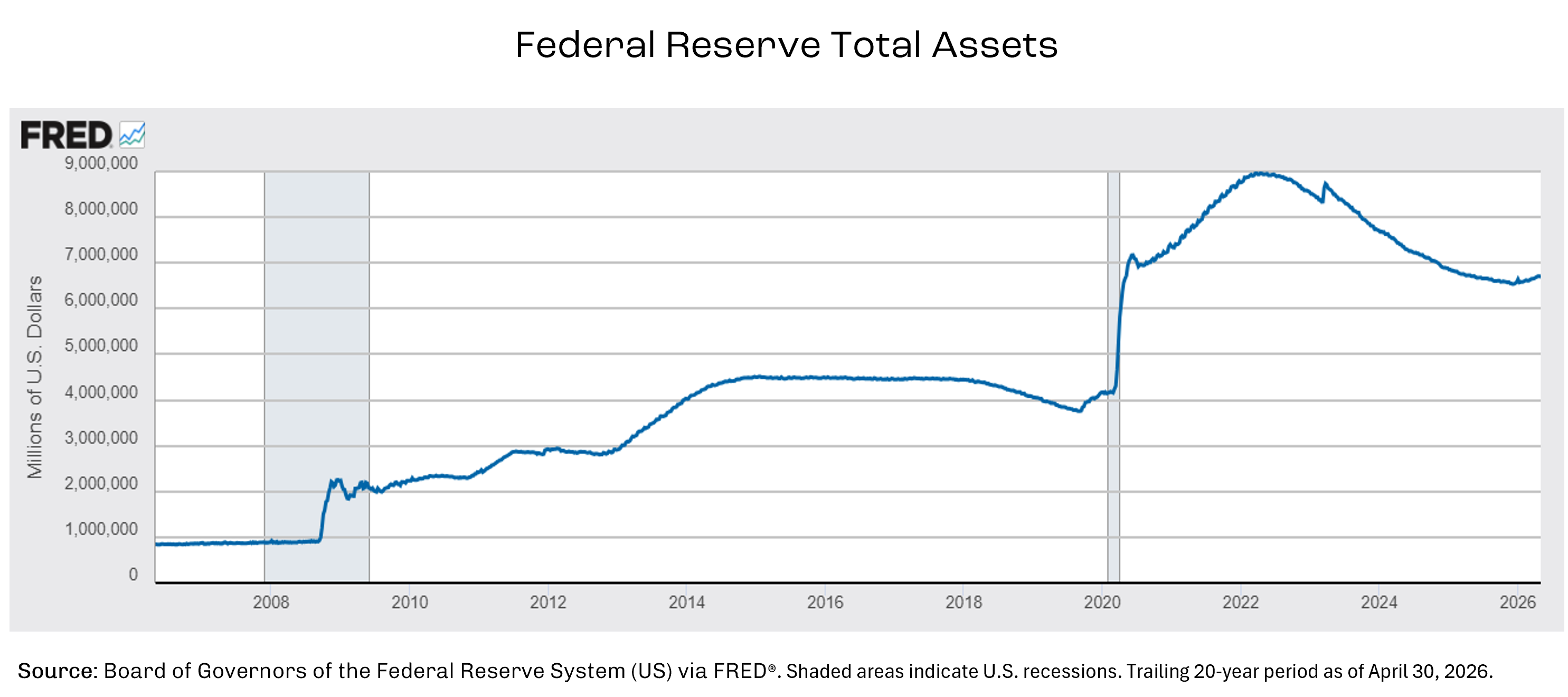

Second, Warsh has expressed concern that the Fed became too reliant on extraordinary policy tools after the Global Financial Crisis (“GFC”) and the pandemic. The most visible example is the balance sheet. Before the GFC, the Fed’s balance sheet was much smaller and was used primarily to implement monetary policy through short-term interest rate operations. After the GFC, and again during the pandemic, the Fed purchased large quantities of Treasury securities and agency mortgage-backed securities to stabilize markets, lower longer-term borrowing costs, and support the economy. These tools were originally framed as crisis responses, but over time they became a recurring part of the policy toolkit.

Warsh’s concern is that repeated use of these tools can change market behavior. If investors believe the Fed will routinely intervene when markets become strained, risk-taking may increase, market discipline may weaken, and asset prices may become more dependent on policy support. In that framework, a large balance sheet is not just a technical issue; it is a signal about the Fed’s role in capital markets. A smaller balance sheet would represent an effort to reduce the Fed’s footprint and return more price discovery to private markets.

The bond market implications are noteworthy. If the Fed allows its Treasury and mortgage-backed securities holdings to decline, private investors must absorb more of that supply. To do so, they may demand a higher term premium, meaning additional compensation for holding longer-duration bonds. That could keep longer-term yields elevated even if the Fed eventually cuts short-term rates. The impact could be most visible in Treasury yields, mortgage rates, municipal bonds, and longer-duration fixed income. A Warsh Fed might therefore be associated with a more complicated rate environment: easier policy at the front end of the curve, but not necessarily a proportional decline in long-term borrowing costs.

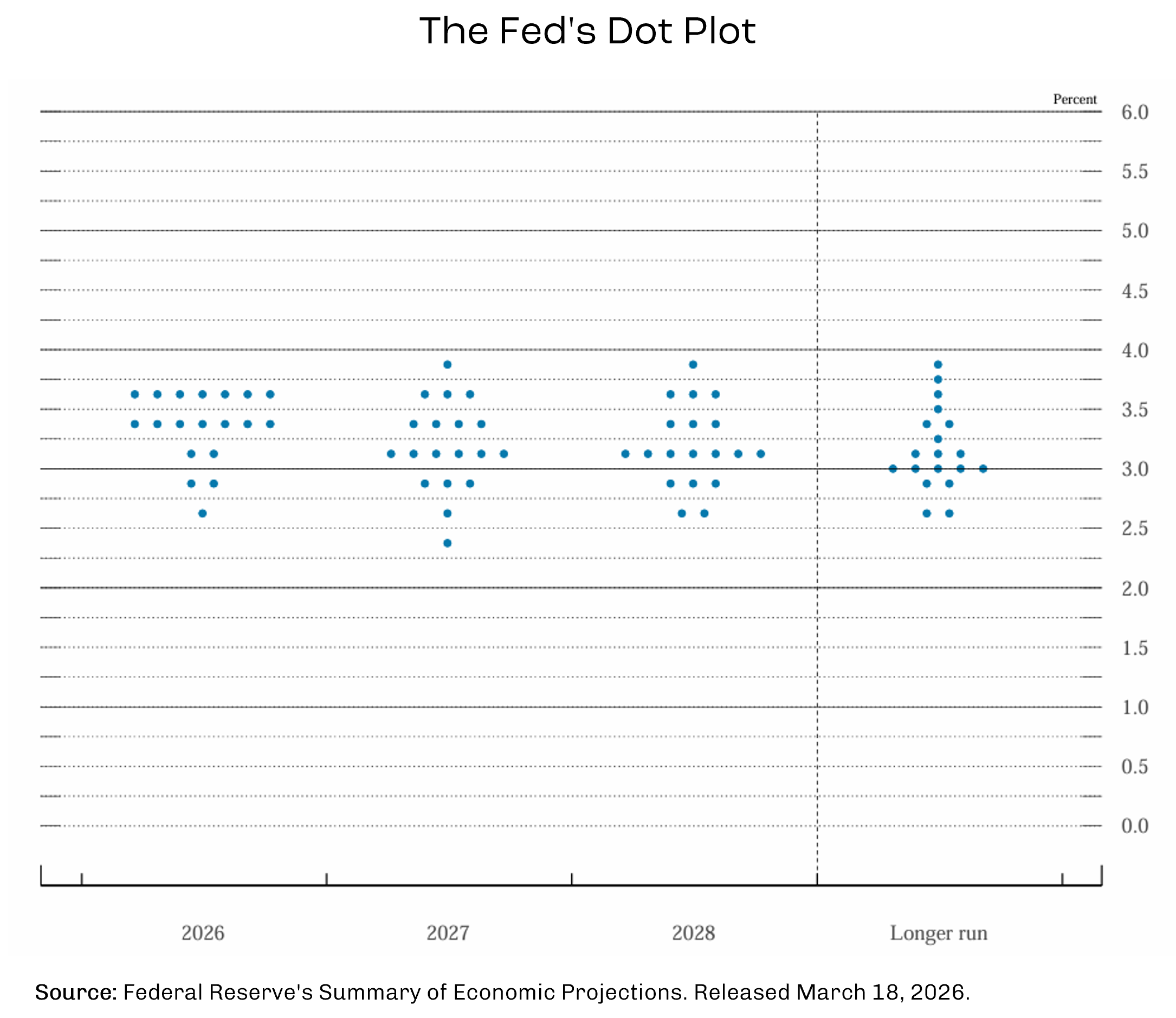

Third, Warsh has suggested that the Fed should communicate less and rely less heavily on forward guidance. Over the last several decades, the Fed has become increasingly transparent. It now uses post-meeting statements, press conferences, speeches, meeting minutes, economic projections, and the “dot plot” to help markets understand how policymakers are thinking. That transparency can reduce uncertainty, but it can also create a different problem. Markets may become overly dependent on Fed signals and may treat guidance as a promise rather than a conditional forecast.

Warsh’s critique is that too much forward guidance can box the Fed in. If policymakers spend weeks preparing markets for a certain decision, they may become less willing to change course when new data arrives. That can reduce the value of live debate at Federal Open Market Committee (“FOMC”) meetings and make policy feel pre-negotiated. Warsh has indicated that he prefers a more flexible process, where officials arrive at meetings prepared to argue different views and make decisions based on the most current information rather than on a path that markets already expect.

For investors, this could represent a meaningful change in the Fed-market relationship. A less scripted Fed may be more adaptive, but it may also be less predictable. Markets have grown accustomed to the Fed trying to avoid surprises. If that changes, policy meetings could become more market-moving, economic data releases could carry greater weight, and interest rate volatility could rise. This does not necessarily mean policy would be less disciplined. It means the Fed may be less willing to smooth every transition for investors in advance.

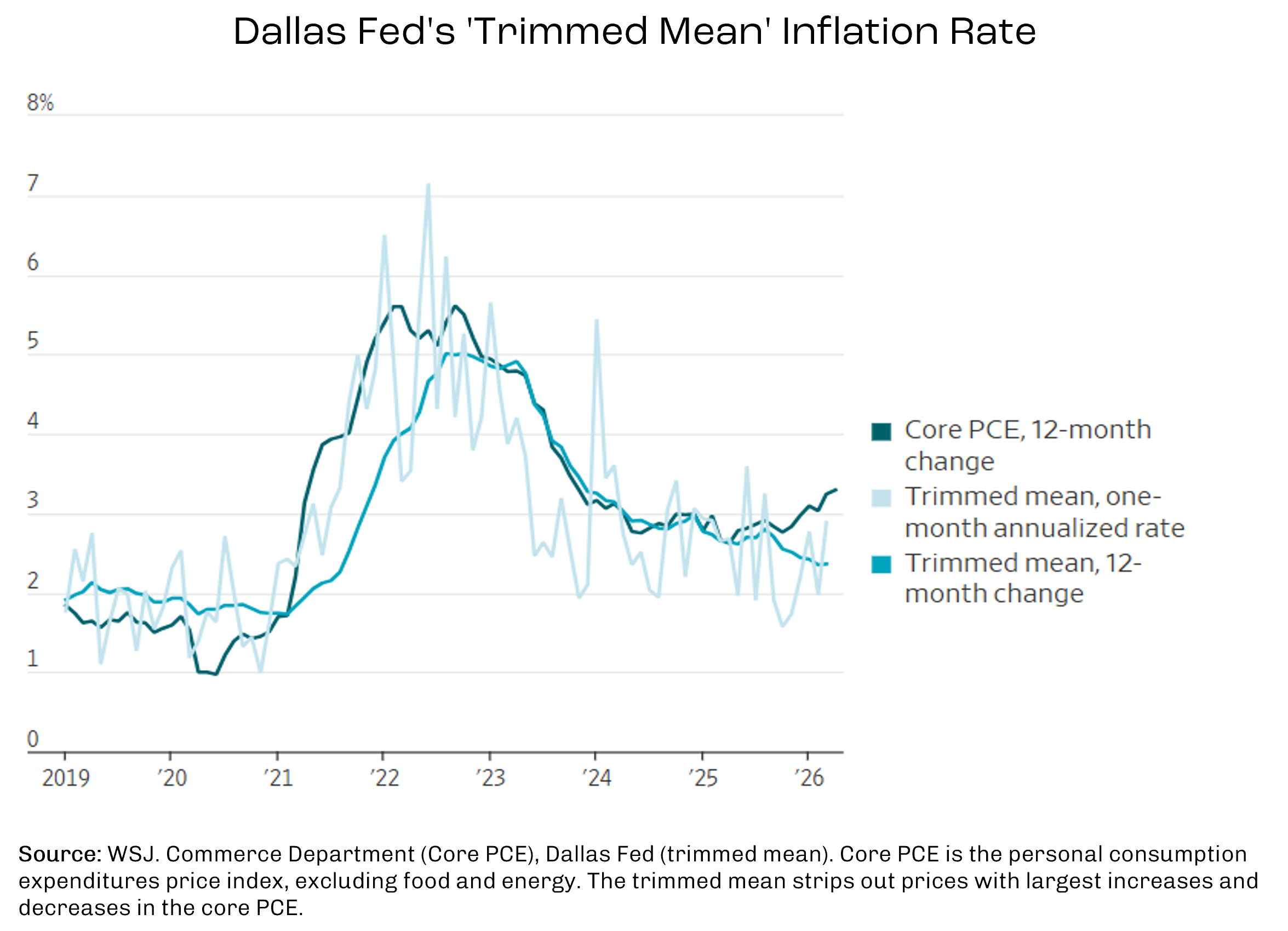

Fourth, Warsh has questioned whether traditional inflation measures always capture the underlying inflation trend. The Fed has historically placed significant emphasis on measures such as the Consumer Price Index (“CPI”) and the Personal Consumption Expenditures (“PCE”) Price Index, particularly core measures that exclude food and energy. Warsh has suggested that policymakers should look more carefully at whether these standard measures give an accurate picture of underlying inflation, especially when the economy is being affected by supply shocks, technological change, productivity shifts, or large relative price moves.

One alternative he has referenced is trimmed mean inflation, which removes the most extreme price increases and decreases before calculating the inflation trend. The purpose is not to ignore inflation that consumers experience, but to separate broad, persistent inflation pressure from temporary or idiosyncratic price swings. For example, a sharp move in energy prices, used car prices, or a narrow technology category could distort headline or even core inflation for a period. A trimmed mean measure may help policymakers ask whether inflation pressure is broadening across the economy or concentrated in a few categories.

This may sound technical, but it matters for policy. If one inflation measure suggests inflation is sticky while another suggests underlying pressure is easing, policymakers could reach different conclusions about whether interest rates are too high, too low, or appropriately restrictive. Warsh also appears interested in more forward-looking analysis, including how productivity growth, artificial intelligence, supply-side improvements, and changes in business investment could affect the economy’s inflation potential over time. That could make the Fed less mechanical in its response to backward-looking inflation data, but it could also make the reaction function harder for markets to read.

Taken together, these priorities point to a Fed that may seek to do less, say less, and rely less on emergency tools. That does not mean policy will automatically be easier or tighter. It means the policy framework itself may become less predictable for investors who became accustomed to a highly communicative Fed with a large market presence. The central question is whether Warsh can translate those preferences into actual policy. The Fed remains a committee-driven institution, and the economic backdrop will ultimately matter as much as the chair’s philosophy.

It is important not to overstate what any Fed chair can do alone. The Fed chair is highly influential, but the Fed is not designed to operate as a one-person institution.

Today, the FOMC is the central body responsible for open-market operations and for the policy decisions that influence the federal funds rate. The committee includes the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven Reserve Bank presidents, who serve one-year voting terms on a rotating basis. Nonvoting Reserve Bank presidents also attend FOMC meetings, participate in the discussion, and contribute to the Committee’s assessment of the economy and policy options.

However, that committee structure was not always how the Fed worked. When the Fed was created in 1913, the system was more decentralized. The founders viewed the Fed as a network of regional Reserve Banks operating with a meaningful degree of local autonomy, subject to oversight from the Federal Reserve Board in Washington. In the early years, open-market operations were not centrally controlled in the same way they are today. Individual Reserve Banks could conduct open-market transactions for their own accounts, which meant monetary policy could be less coordinated across districts.

That decentralized structure became increasingly difficult to manage. In the early 1920s, the Reserve Banks began coordinating more formally because actions taken by one Reserve Bank could affect financial conditions in other districts. This led to the creation of committees designed to coordinate open-market purchases and sales. By the early 1930s, however, the limits of voluntary coordination had become apparent. During the Great Depression, disagreements among Reserve Banks contributed to inconsistent policy responses, and Congress moved to centralize open-market authority.

The Banking Act of 1933 created the Federal Open Market Committee and made its decisions binding on the Reserve Banks. The Banking Act of 1935 then created the basic modern structure of the FOMC: the Board of Governors, the New York Fed president, and four other Reserve Bank presidents voting on a rotating basis. This reduced the ability of individual Reserve Banks to pursue independent open-market policies and moved the Fed toward a more nationally coordinated monetary policy framework.

This helps explain the balance built into the modern Fed. The Board of Governors gives the system national policy direction and political accountability through presidential appointment and Senate confirmation. The Reserve Bank presidents bring regional economic intelligence and independent institutional perspectives. The New York Fed has a permanent voting role because it implements open-market operations through its trading desk and is closest to the functioning of financial markets.

The chair sits at the center of this structure. They set the tone, frame the debate, lead the press conference, influence staff priorities, and often plays the most important role in building consensus. Historically, some Fed chairs have exercised that role very forcefully, using agenda control, communications, and institutional authority to guide the Committee toward a preferred policy outcome. In practice, therefore, the chair can be much more influential than a simple one-vote description would suggest.

But the chair still has one vote. Major monetary policy shifts require support from the broader committee. That distinction is especially important under Warsh. He may be able to change the Fed’s process, tone, communication style, and policy emphasis relatively quickly. But changing the actual direction of monetary policy requires persuading other voting members, especially when inflation risks, labor-market risks, and financial-stability concerns are pulling policymakers in different directions.

The current committee is not necessarily aligned around aggressive rate cuts. At the April 2026 FOMC meeting, the Committee voted to hold the federal funds target range steady, but the vote revealed disagreement over both policy direction and communication. Stephen Miran dissented because he preferred a 25 basis point rate cut. Beth Hammack of the Cleveland Fed, Neel Kashkari of the Minneapolis Fed, and Lorie Logan of the Dallas Fed supported holding rates steady but dissented because they opposed including an easing bias in the statement.

Hammack, Kashkari, and Logan were not dissenting because they wanted higher rates at that meeting. They dissented because they believed the statement leaned too much toward future easing at a time when inflation risks remained elevated. In other words, their objection was about the Fed’s forward guidance and policy signal, not the immediate decision to leave rates unchanged.

Those three Reserve Bank presidents are 2026 voters, but they are scheduled to rotate out of voting seats in 2027. Under the Fed’s published rotation schedule, the 2027 voting Reserve Bank presidents will come from New York, Chicago, Richmond, Atlanta, and San Francisco. That means Cleveland, Minneapolis, and Dallas will not have voting seats in 2027 unless there are personnel or structural changes.

However, rotating off the voting roster does not mean leaving the policy process. Reserve Bank presidents who are not voting members still attend FOMC meetings, participate in the discussion, present their regional economic assessments, and help shape the debate. They can also influence expectations through speeches, interviews, research, and public commentary. So while the formal voting arithmetic may become less hawkish after 2026 if those dissenters rotate off, their views will not disappear from the room.

Meanwhile, Board governors remain voting members. Board seats do not rotate annually. If Warsh wants to move policy meaningfully toward faster rate cuts, a smaller balance sheet, less forward guidance, or a different inflation framework, he will need to build support among the other governors and the voting Reserve Bank presidents. The rotating Reserve Bank seats can change the tone of a given year’s FOMC, but the Board of Governors provides continuity.

The practical takeaway is that the Fed may become more debate-oriented under Warsh, but that does not guarantee a rapid policy pivot. The modern FOMC was designed to centralize policy authority while preserving a mix of national and regional perspectives. Warsh can influence the institution, but he still has to lead it through persuasion, consensus-building, and the formal voting structure of the Committee.

One of the most important issues for investors is the relationship between short-term rates and long-term rates. The Fed directly influences very short-term interest rates through its policy rate. Long-term Treasury yields, mortgage rates, and corporate borrowing costs are influenced by Fed policy, but they are also shaped by inflation expectations, fiscal deficits, term premiums, global capital flows, and supply-and-demand dynamics in bond markets.

This is where Warsh’s balance sheet views become especially important. If the Fed cuts short-term rates while also pursuing a smaller balance sheet, the yield curve may not respond in a simple or uniform way. Short-term yields could fall if the Fed eases policy, while longer-term yields could remain elevated or even rise if investors believe inflation risks are not fully contained or if the Fed is reducing its role as a large buyer and holder of longer-duration securities.

That combination would be unusual for clients expecting “Fed cuts” to automatically translate into lower borrowing costs across the economy. Mortgage rates, municipal yields, and longer-term corporate borrowing costs may not fall as much as the federal funds rate if the bond market demands a higher term premium.

A Warsh Fed could try to lower the front end of the yield curve while shrinking the Fed’s presence in the back end. Whether that produces easier financial conditions depends on how investors interpret inflation, credibility, and Treasury and mortgage-backed securities supply.

For diversified investors, the main takeaway is not that Warsh is “good” or “bad” for markets. It is that the Fed’s reaction function may become less predictable. A less communicative Fed could mean more volatility around meetings. A smaller balance sheet could mean more attention to Treasury supply, mortgage-backed securities, and liquidity in funding markets. A renewed focus on the Fed’s core mandate could reduce the probability of policy support being extended to every market disruption, unless financial stability is clearly at risk.

At the same time, institutional constraints remain meaningful. The Fed is not a one-person institution. The chair must build consensus, respect incoming data, and preserve credibility with markets. If inflation remains above target, rate cuts may be difficult to justify. If growth slows sharply or financial conditions tighten abruptly, the committee may respond differently than Warsh’s prior comments would suggest.

That is why investors should be cautious about drawing straight lines from a new Fed chair to a specific market outcome. Fed leadership matters, but economic conditions, inflation data, fiscal policy, and market functioning will matter at least as much.

Over the coming months, we are watching five areas. First, the tone of the June FOMC meeting and press conference. This will provide an early read on whether Warsh emphasizes continuity, reform, or a more immediate policy shift. Second, the balance sheet discussion. The pace, composition, and communication of any balance sheet reduction plan could matter for long-term yields. Third, dissents and committee language. More dissents may signal a less consensus-driven Fed, which could increase policy uncertainty but also provide more transparency into internal debate. Fourth, inflation interpretation. If the Fed places more weight on alternative inflation measures, markets will need to adjust to a potentially different framework for evaluating policy decisions. Fifth, the relationship between short-term and long-term rates. If short-term rates fall while long-term rates remain sticky, the market may be telling us that policy credibility, inflation risk, or Treasury supply are still concerns.

Kevin Warsh may bring a meaningful change in style and policy emphasis to the Fed. He appears likely to favor a smaller Fed footprint, less forward guidance, stricter focus on the central bank’s mandate, and greater scrutiny of how inflation is measured.

But investors should separate policy preference from policy implementation. The Fed operates through committees, formal votes, institutional norms, and incoming economic data. Warsh can shape the debate, but he cannot single-handedly dictate the outcome.

For clients, the practical implication is to prepare for a potentially less predictable Fed rather than to assume a simple rate-cut playbook. The path of interest rates may become more differentiated, with short-term rates, long-term yields, mortgage rates, and credit spreads responding to different forces.

As always, portfolio decisions should be grounded in long-term objectives, risk tolerance, liquidity needs, and diversification rather than in any single policy transition. A new Fed chair can change the conversation, but disciplined portfolio construction remains the more durable foundation.

.png)

.png)