Written by

Michael J. Firestone, CFA

Written by

Michael J. Firestone, CFA

Published on

July 9, 2026

Category

Market Trends & Commentary

.png)

Markets and the economy entered the second half of 2026 on firmer footing than many expected, supported by resilient consumer spending, stable employment, strong corporate profits, fiscal support, and a powerful AI-related capital spending cycle. This does not look like an economy on the edge of a traditional recession, but the central theme is resilient, but more dependent: growth and markets are growing increasingly sensitive to policy, energy prices, AI investment, earnings concentration, and the Fed’s changing communication framework. In this environment, understanding what is inside a portfolio matters as much as the headline allocation.

1. The economy remains resilient

Consumer spending, fiscal support, corporate profits, and AI-related capital spending continue to support growth. The labor market remains stable, though hiring has slowed from earlier in the expansion.

2. The World Cup provides a timely boost

The event should temporarily support payrolls, retail sales, tourism, hotels, restaurants, and transportation, while also offering a harder-to-measure lift to sentiment and global perception.

3. Inflation has improved, but upside pressure is evident

Lower oil prices should help ease headline inflation pressure, but core inflation remains sticky. New bottlenecks tied to AI infrastructure, including memory, power, data centers, and specialized labor, may keep parts of inflation more complicated than the headline numbers suggest.

4. Earnings are carrying more of the market’s weight

Equity gains have been supported by strong earnings, not just valuation expansion. However, much of the momentum remains tied to technology, semiconductors, energy, and AI-related capital spending, leaving markets more sensitive to a concentrated group of leaders.

5. AI still has room to run, but the easy phase may be behind us

AI remains a powerful long-term theme, but the next phase will likely require evidence of revenue conversion, enterprise adoption, free cash flow discipline, and attractive returns on capital. The opportunity remains significant, but execution risk is rising.

We enter the second half of 2026 with markets and the economy on firmer footing than many expected earlier in the year. The economy has remained resilient, corporate profits have continued to grow, and the artificial intelligence investment cycle remains one of the most powerful forces supporting capital spending, earnings, and market sentiment.

At the same time, the sources of resilience have become more concentrated. Consumers are still spending on the aggregate, but not all households are drawing from the same foundation. Some have benefited from the wealth effect with rising portfolio values providing increased spending power, while others remain more exposed to inflation, interest rates, and reduced savings cushions. Lower oil prices should help to ease headline inflation pressure, but elevated core inflation may be sticky throughout 2026 in part due to AI-related bottlenecks and World Cup related regional pricing distortions. Corporate earnings remain strong, though a meaningful share of earnings momentum is tied to technology, energy, and AI-related capital spending. Policy uncertainty is also rising as markets adjust to a new Federal Reserve Chair, a changing Fed communication style, unresolved geopolitical risks around Iran, and the approaching U.S. midterm elections.

This is not an environment that appears fragile in the traditional recessionary sense. It is, however, one that has become more sensitive to a narrower set of supports, including policy stability, energy price stability, continued AI investment, and earnings growth from a concentrated group of market leaders.

On the aggregate, the consumer has remained resilient despite several years of elevated prices and higher interest rates. Spending has continued, household balance sheets remain stronger than many feared, and sentiment has recently improved as markets recovered and inflation pressures eased in some areas. The labor market is also best described as sturdy but slowing: still supportive of consumption, but no longer as uniformly strong as it was earlier in the expansion.

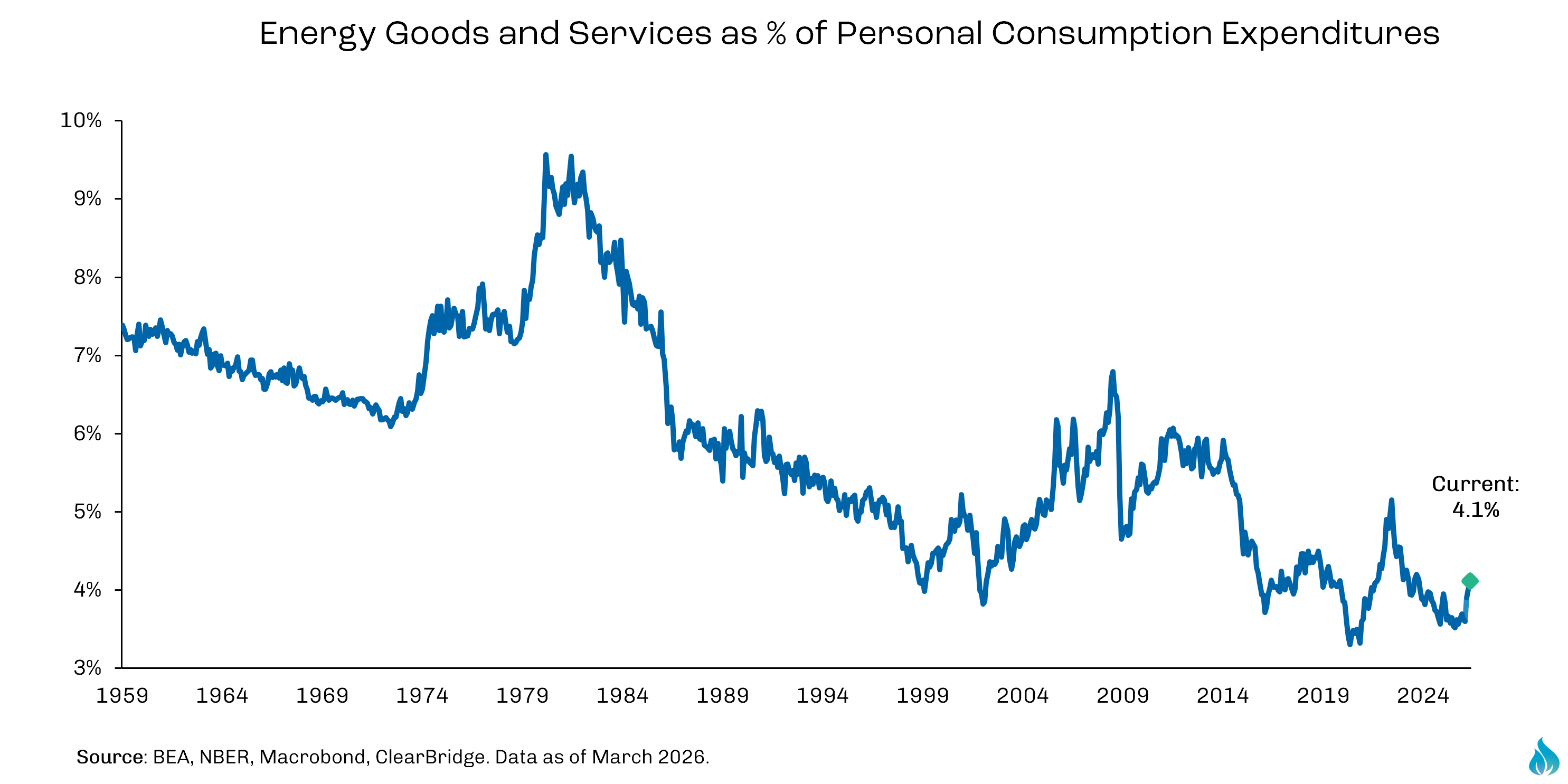

Inflation remains the most important economic crosscurrent. Lower oil prices should reduce pressure on headline inflation at an important moment, and the U.S.-Iran agreement has reduced the risk of a more disruptive energy shock. That relief matters for consumers and for Fed policy.

However, the inflation story is not fully resolved. Core inflation remains sticky, services prices are still firm, and new bottlenecks are emerging in areas tied to the AI buildout. This is different from the post-pandemic inflation cycle, which was driven more by stimulus, supply chain disruption, and shelter-in-place driven consumer demand. Today’s inflation risk is narrower but still important: when many companies compete for the same scarce inputs, prices can rise even if the overall economy is not overheating.

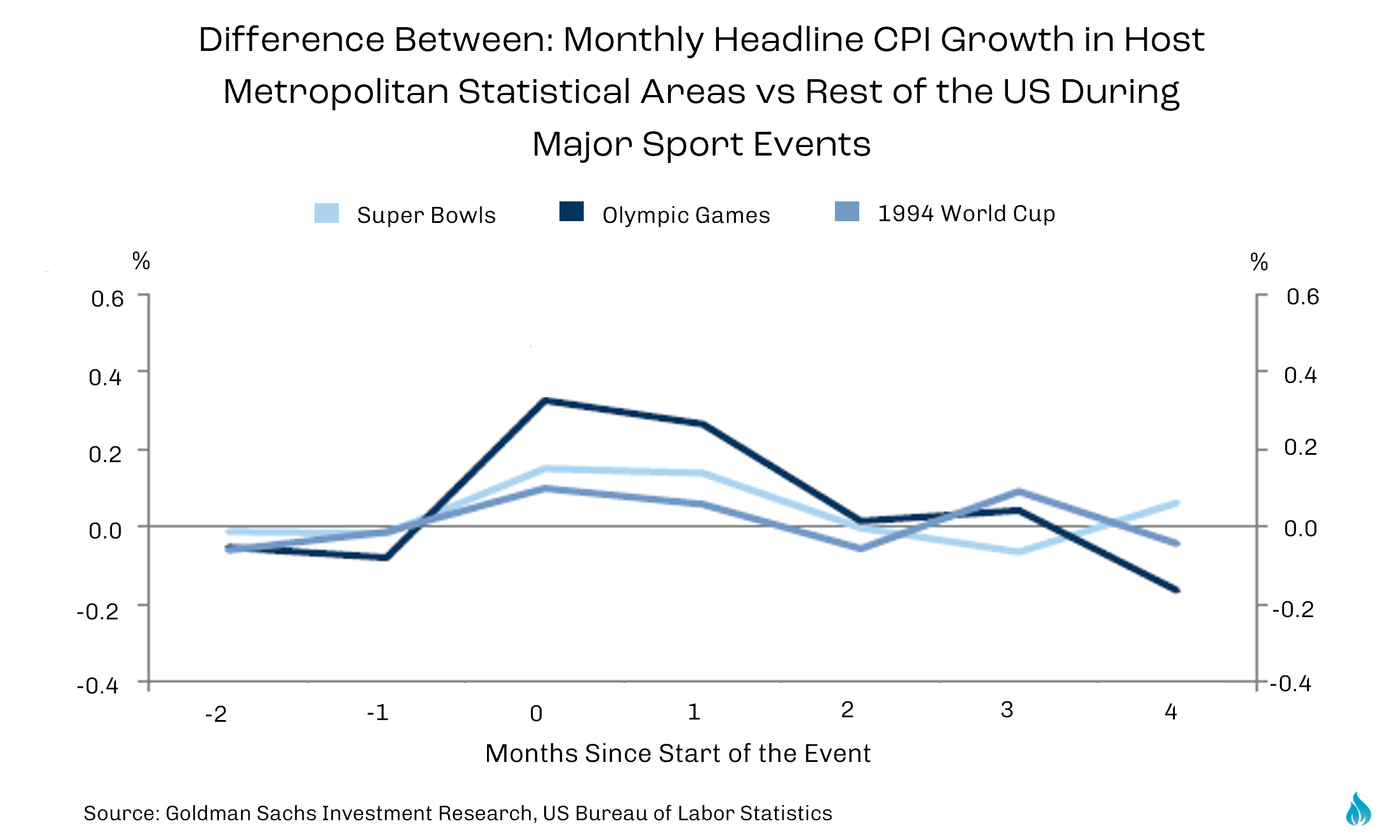

One unusual and timely contributor this quarter is the World Cup. It is tempting to treat a sporting event as a fun side story, but the 2026 World Cup is large enough to matter for short-term economic data. Goldman estimates that the U.S. will host 78 matches across 11 metropolitan areas, with 5-6 million attendees. Those host cities represent roughly 32% of U.S. GDP, 23% of total employment, and 26% of the CPI index. Goldman estimates the tournament could add 40,000 jobs to June payrolls and another 10,000 in July, with some payback beginning in August as temporary hiring unwinds. The estimated effect on retail sales is also meaningful for a monthly data series, with Goldman estimating a 0.3 percentage point boost in June and a 0.1 percentage point boost in July.

The World Cup has also affected tourism expectations. After inbound foreign tourism declined in 2025, 2026 estimates have improved, helped by expectations for more than 1.24 million international World Cup visitors. This may be best viewed as a temporary boost for now, but the overwhelmingly positive feedback from visitors and social media may also help shift international perception in a way that supports future tourism demand. The impact is difficult to measure, but countries, like companies, benefit when the experience they deliver exceeds expectations.

The tournament also complicates the inflation picture. Goldman estimates the World Cup could add 0.03 percentage points to June core CPI and 0.04 percentage points to June core PCE, with another small boost in July and some payback beginning in August. Past major sporting events have pushed host-city prices higher, particularly in hotels, restaurants, and transportation. This does not mean the World Cup creates a new inflation regime. It does mean inflation data is sensitive to misinterpretation which has meaningful policy and market implications if assessed incorrectly.

At a time when the public conversation has been dominated by war, politics, inflation, and immigration, the World Cup offers something different: packed stadiums, foreign visitors, city-level energy, and a reminder that the United States remains one of the world’s most dynamic places to gather. Economists can estimate hotel prices, restaurant spending, and retail sales. It is harder to quantify a country’s “vibe.” The tournament has offered a refreshing form of positive nationalism, with nations rallying around sport rather than fear. Particularly in the U.S., the World Cup has arrived at a moment when many people seem eager for something shared to rally around. As the country celebrated its 250th anniversary, that sense of shared experience may have provided a much needed lift, whether we realized it or not. Pride in country does not require agreement with every policy, leader, or decision. It can also reflect something deeper: an appreciation for the ideals we continue to pursue, the communities we belong to, and the moments that remind us we are still capable of coming together.

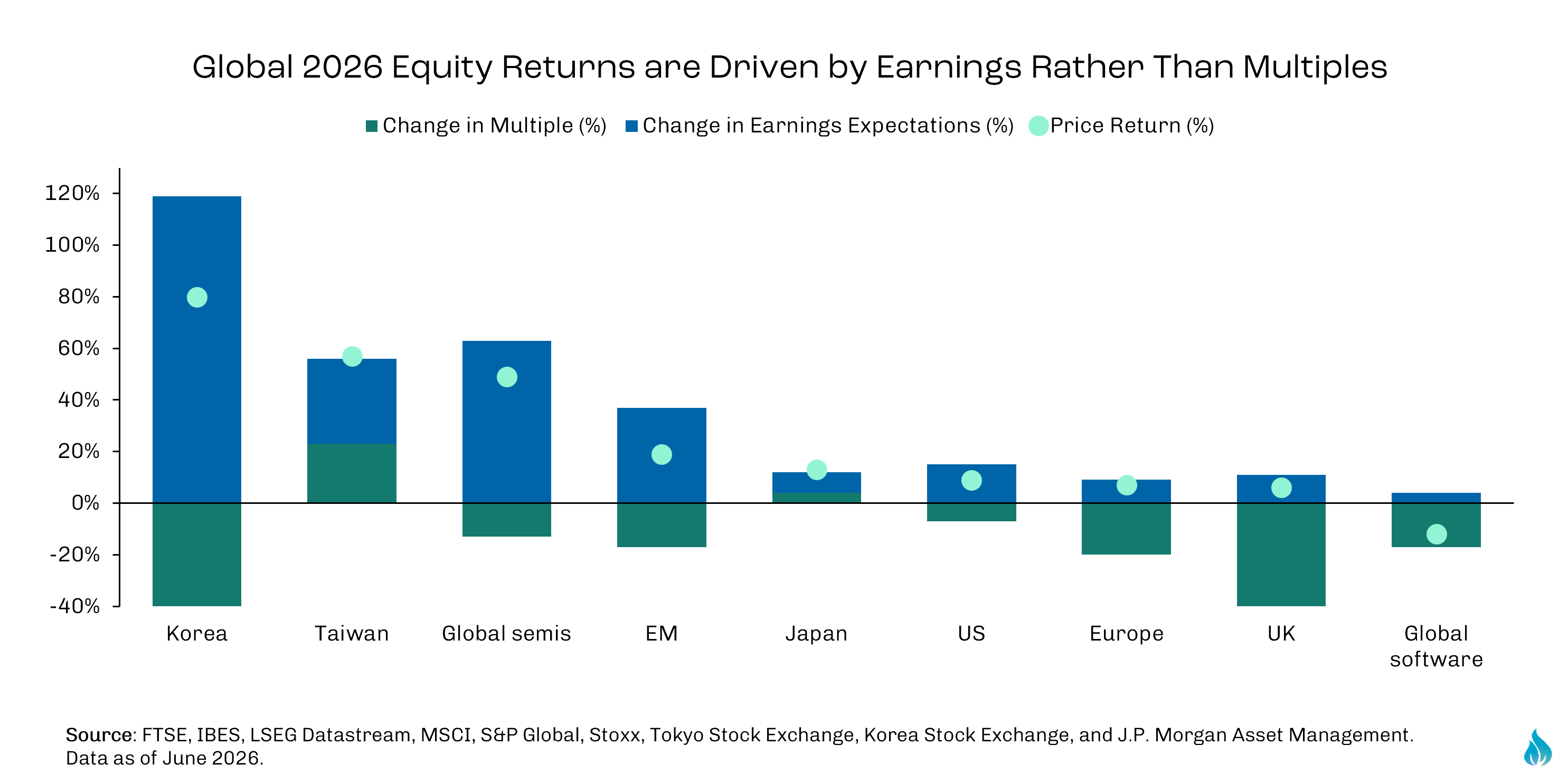

The equity market has continued to rise, but importantly, it has not been driven by valuation expansion alone. Earnings have done a meaningful share of the work. FactSet estimates S&P 500 earnings growth of 23.1% for Q2 2026, which would mark the second consecutive quarter of earnings growth above 20%. Revenue growth is expected to be 12.3%, the strongest since Q2 2022 if realized. FactSet also notes that earnings estimates have increased during the quarter, which is unusual because analysts typically reduce estimates as reporting dates approach.

Strong markets are easier to defend when prices rise alongside earnings. Since the end of Q1, FactSet reports that the S&P 500 price increased 12.7%, while forward 12-month EPS estimates rose 10.4%. Valuations remain full, but they are more supported than they would be if prices were rising while earnings expectations stagnated. The forward 12-month P/E ratio of 20.1 is generally in line with the 5-year average of 19.9 and the 10-year average of 19.0.

Sector leadership remains important. FactSet expects ten of eleven sectors to report year-over-year earnings growth, led by Energy, Information Technology, and Materials. The Information Technology sector is expected to deliver earnings growth of 63.2%, with semiconductors and semiconductor equipment expected to grow 131%. Excluding semiconductors, expected Information Technology earnings growth would fall from 63.2% to 25.7%.

That statistic captures much of the current market environment. Earnings are strong, but the engine is still highly dependent on the AI supply chain. Semiconductors, memory, hardware, power, electrical equipment, and cloud infrastructure are doing a great deal of the heavy lifting. Market breadth has improved in places, and areas that lagged earlier in the cycle have participated more recently, but the earnings story is still tied closely to AI-related demand.

This creates a subtle but important risk. AI does not need to fail for market concentration to matter. It only needs to stop exceeding expectations. When index weightings, earnings revisions, capital spending plans, and investor enthusiasm all depend on the same theme, small disappointments can matter.

Index construction adds another layer. If large private AI-related companies go public over the next several years, passive funds may be required to purchase them based on index methodology. Those purchases are not additive in isolation. Existing holdings must make room. Depending on the index provider, a company could enter one benchmark quickly, another after a seasoning period, and another only after committee approval. In a world where passive exposure is large, “owning the market” may increasingly mean owning a changing mix of public and newly public AI-related companies.

The most important near-term policy shift is at the Federal Reserve. Kevin Warsh’s first FOMC meeting was notable less because rates changed and more because the Fed’s tone and communication style changed. Piper Sandler summarized the meeting with three key takeaways: the FOMC appears more concerned about inflation than expected, the Chair is emphasizing price stability while pulling back from characterizing the full Committee view, and the Fed announced five task forces focused on communications, the balance sheet, data sources, productivity/AI/jobs, and the inflation framework.

The June meeting was hawkish in tone. The FOMC statement ended with the phrase “The Committee will deliver price stability,” and the median 2026 core PCE projection rose from 2.7% to 3.3%. Piper Sandler notes that the central tendency of core inflation projections now runs from 3.2% to 3.5%.

Still, hawkish communication does not automatically mean rate hikes are necessary or imminent. Piper Sandler also notes that reaching the Fed’s median 2026 core PCE projection still requires inflation to decelerate over the second half of the year, with annualized core PCE needing to slow to roughly 2.7% from June through December. Their view remains that the Fed can stay on hold if incoming inflation data makes that slowdown plausible.

The bigger market implication may be volatility. Warsh appears more willing to speak narrowly, reduce forward guidance, and allow more uncertainty around the Committee’s reaction function. That may make each inflation print, labor report, and Fed speech more market-moving. In plain English, the market may be moving from a Fed that tried to prepare investors for every turn in the road to a Fed that is more willing to let investors drive through fog.

The balance sheet also deserves attention. The Fed funds rate controls the front end of the yield curve, but the balance sheet can affect the long end through liquidity, Treasury supply absorption, and term premium. A Fed that eventually cuts short-term rates while shrinking the balance sheet could still leave longer-term borrowing costs elevated. That matters for mortgages, municipal bonds, corporate borrowing, and long-duration assets.

Oil is the second catalyst. Futures have fallen back close to pre-war levels as shipping through the Strait of Hormuz continues, reducing fears of a sustained energy-driven inflation shock. Unsurprising, the truce remains fragile, with maritime risks, hostile rhetoric, and unresolved transit disputes still present. Lower oil helps consumers and the Fed, but only if it stays lower. That said, it’s worth noting that today’s domestic economy is less sensitive to oil shocks compared to history. The combination of immense U.S. oil production, broad-based energy efficiency gains, and a complimentary alternative energy supply has reduced the direct impact of energy price fluctuations on the average American consumer.

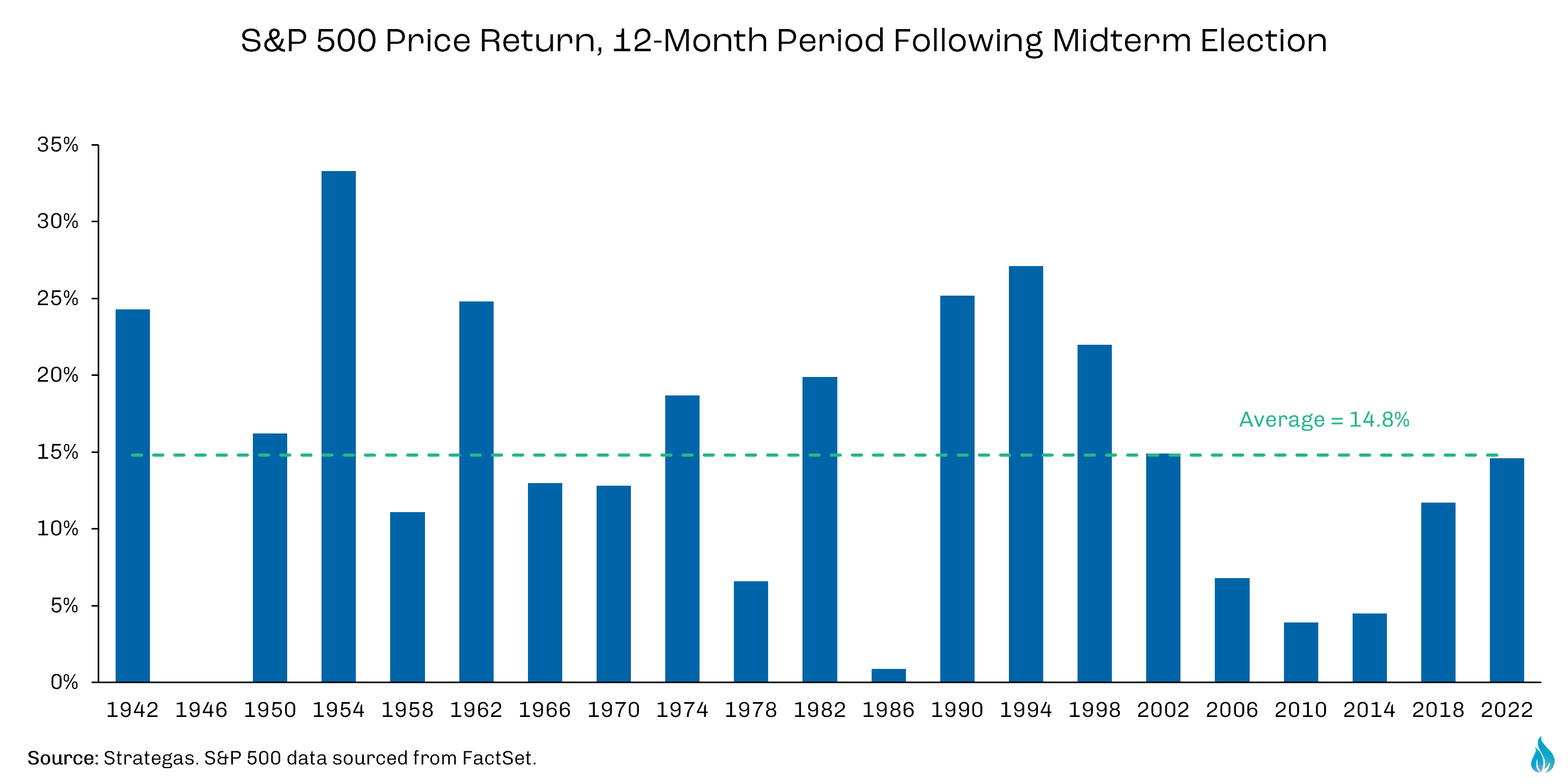

The midterm elections are the third catalyst. The midterm elections are likely to become a more prominent market topic as the year progresses, but history suggests elections are rarely as simple for markets as “one party wins, stocks rise or fall.” Party control can influence tax policy, regulation, health care, energy, infrastructure, defense, and oversight, but broad market returns are usually driven more by earnings, inflation, interest rates, and the economic cycle than by politics alone. Strategas notes that midterm election results have historically been “less of a macro issue” and more important for specific sectors, subindustries, and stocks.

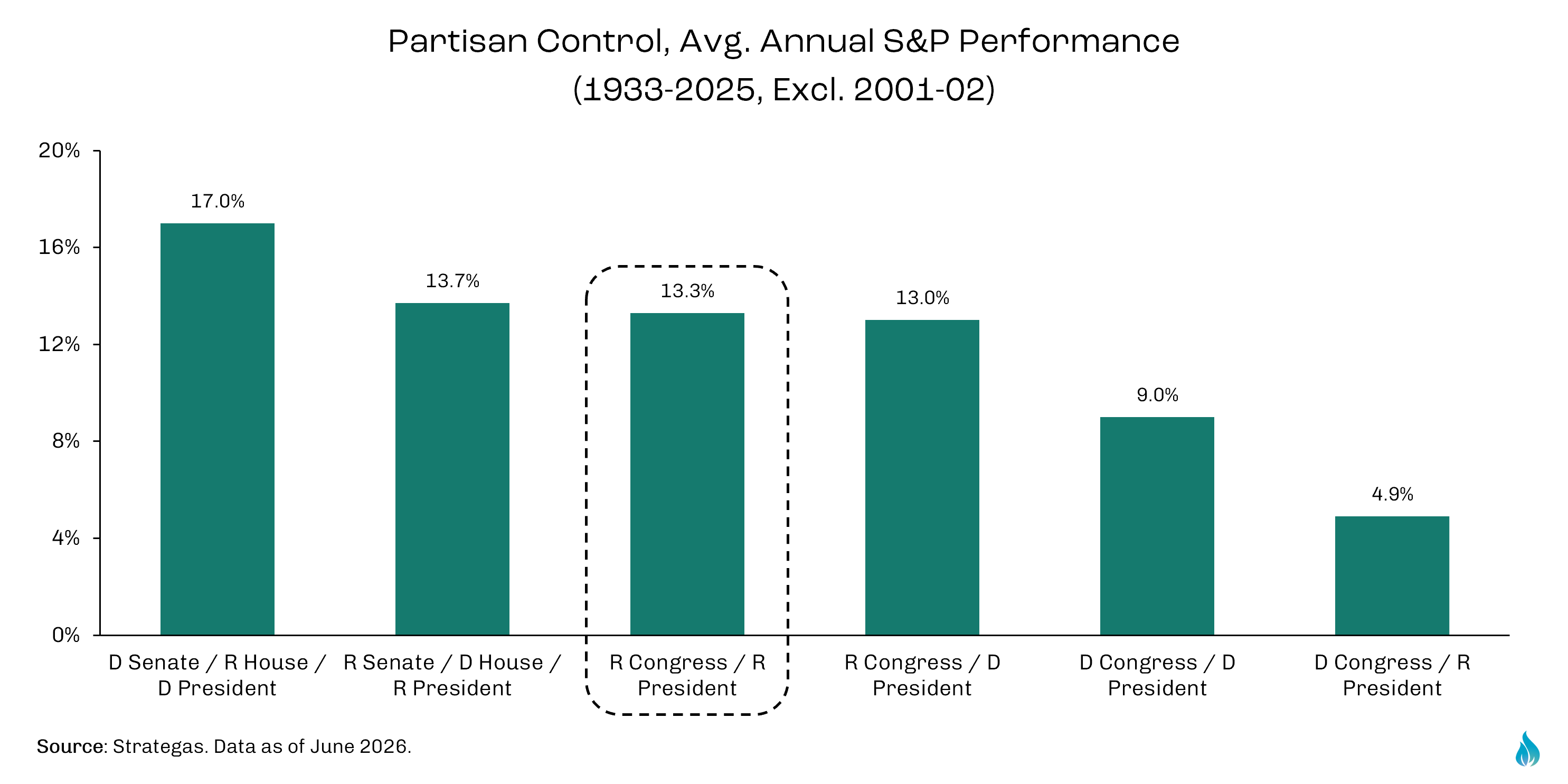

The historical record also argues against treating midterm uncertainty as a reason, by itself, to become materially more defensive. Strategas shows that the S&P 500 has not declined in the 12 months following a midterm election since 1938, with an average 12-month post-midterm price return of 14.8%.

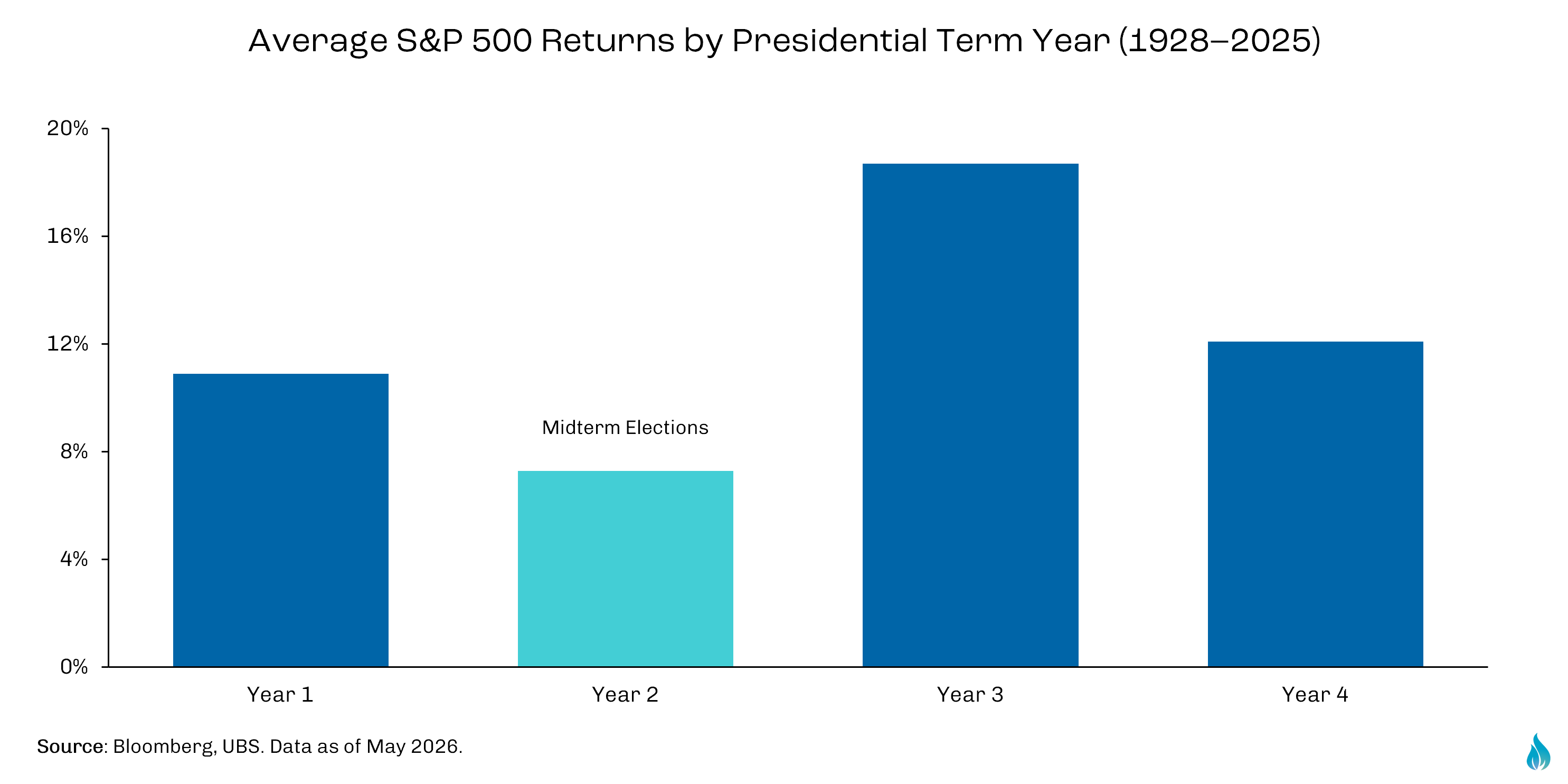

While every cycle has its own economic and policy backdrop, the broader lesson is that markets often dislike uncertainty more than any specific political outcome. Once elections pass, investors can begin analyzing actual policy paths rather than campaign rhetoric. This may be the underlying reason why equity market returns tend to be the lowest in year 2 of the president's 4 year term.

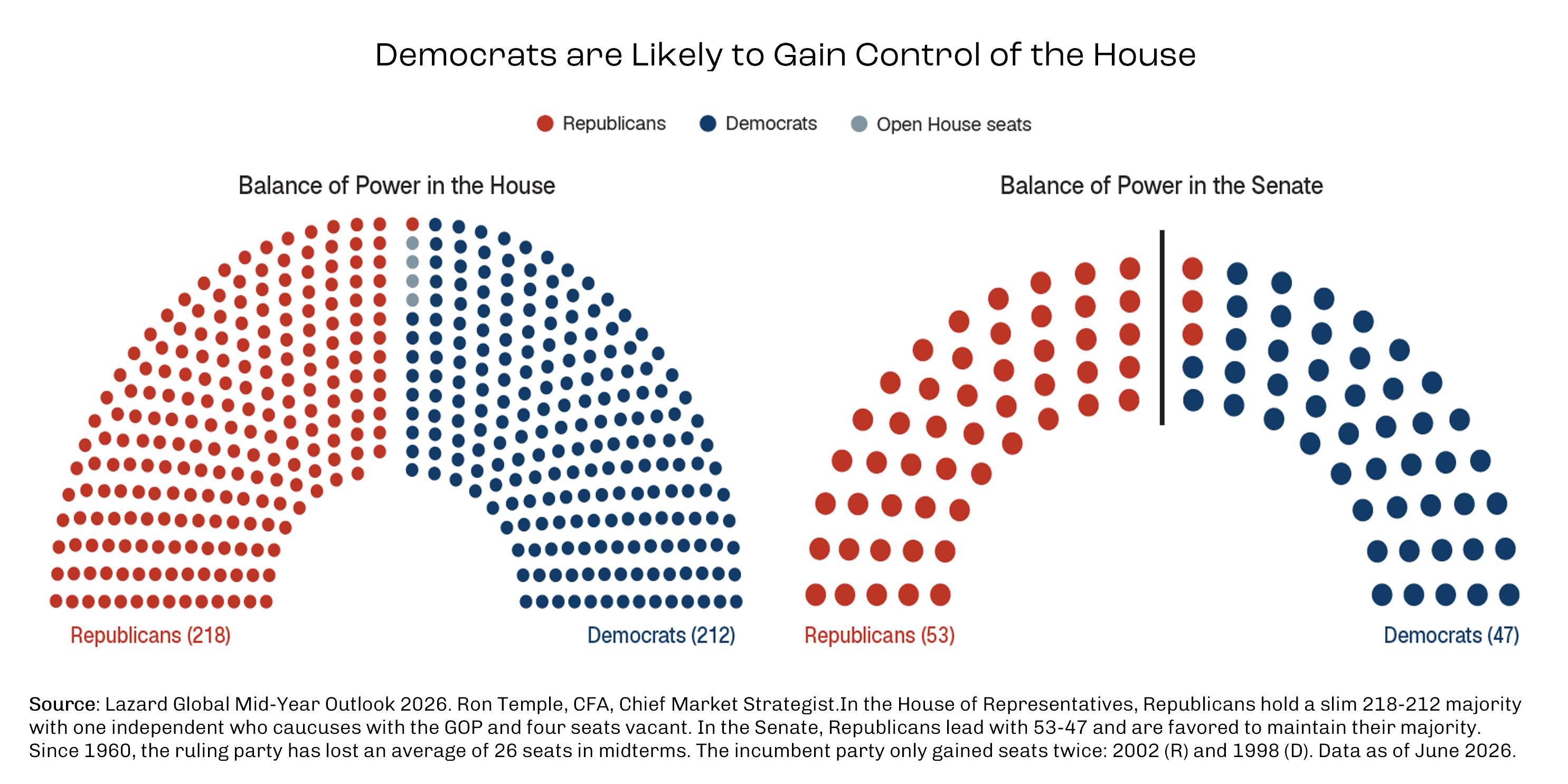

The current setup remains fluid. Strategas notes that prediction-market odds recently implied Democrats could gain the four Senate seats needed to take control, including North Carolina, Maine, Alaska, and Ohio. However, those odds have shifted as oil prices declined, gasoline prices improved, primaries selected candidates, and President Trump’s approval rating bounced from its lows. A plausible outcome is a Republican president and Senate with a Democratic House. That structure would likely limit sweeping legislation, while still leaving room for oversight, budget fights, confirmations, regulatory appointments, and targeted policy compromise.

For markets, the implications would likely be felt more by sector than by the overall index. A Republican Senate could act as a buffer against legislation affecting financials, biotech, credit card fees, and drug pricing, while supporting the administration’s deregulatory and appointment agenda. A Democratic House could use oversight and budget leverage to focus on health care affordability, Medicaid implementation, immigration funding, data centers, crypto, consumer protection, and environmental issues. Health care could be especially sensitive, as Medicaid work requirements and redeterminations under OBBBA are scheduled to begin January 1, 2027, with provider tax changes beginning earlier, creating potential room for negotiation.

Energy, infrastructure, and AI-related power demand may be among the most important areas for potential compromise. A Democratic House would likely seek to protect or expand funding for water, rail, broadband, and renewable priorities, while a Republican Senate would likely emphasize traditional energy, LNG, permitting, defense, and immigration enforcement. Strategas notes that growing data center power needs and concerns about electricity affordability could give both parties a reason to pursue some form of permitting or energy infrastructure compromise. Political rhetoric is likely to intensify in the months ahead, which may translate to heightened market volatility, even before any actual policy changes occur.

Artificial intelligence remains the dominant investment theme of this cycle. It is influencing capital spending, earnings growth, power demand, semiconductor pricing, labor market assumptions, and market concentration. In our view, the AI investment cycle does not appear finished, but it is moving into a more demanding phase. The first stage of the AI trade rewarded possibility. The next stage is likely to require evidence: revenue conversion, enterprise adoption, free cash flow discipline, regulatory clarity, and proof that the enormous infrastructure buildout can earn an attractive return over a reasonable amount of time.

That is why the headwinds deserve attention. Acknowledging these headwinds does not mean dismissing the broader opportunity. It simply means recognizing that technologies this large eventually move beyond the controlled environment of early adoption and into the messier real world of regulation, infrastructure, capital budgets, labor markets, and political scrutiny.

Regulation is one of the clearest examples. Recent reporting indicates that the U.S. government asked OpenAI to restrict the release of a new frontier model to selected partners during a cybersecurity review, while Anthropic also faced temporary restrictions around advanced model access after national security concerns. This does not mean frontier AI development has stopped. It does show that the most capable models are beginning to resemble dual-use technologies, where the same capabilities that create commercial value may also raise national security, cyber, and social risk concerns.

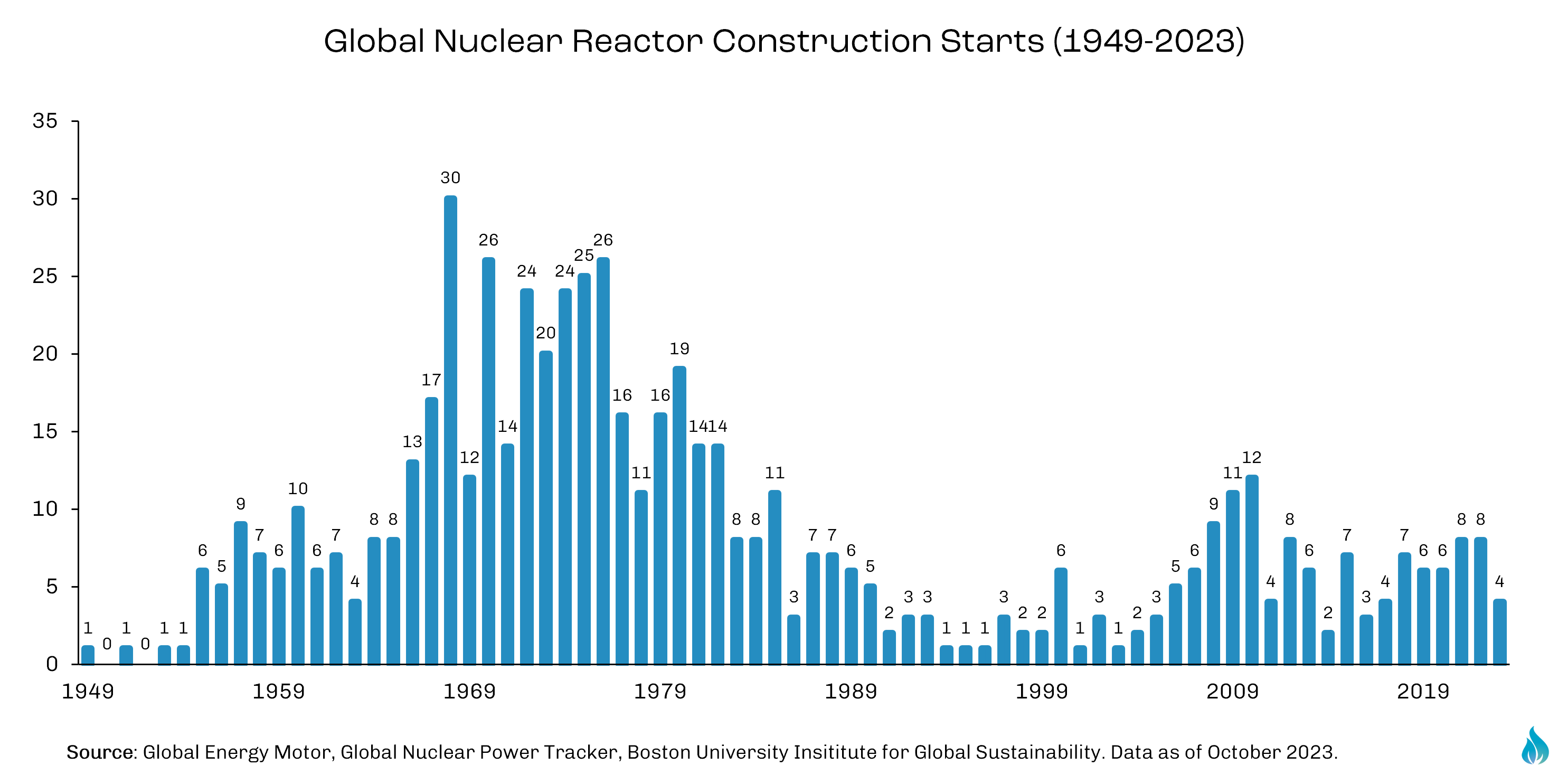

There is historical precedent for this type of tension. Nuclear power had enormous promise after World War II, and global reactor construction accelerated meaningfully in the 1960s and 1970s. Yet the pace of deployment slowed sharply in later decades as safety concerns, public opposition, cost overruns, licensing complexity, and major accidents such as Three Mile Island and Chernobyl changed the regulatory and political environment. AI is not nuclear technology, and the comparison should not be stretched too far. But the analogy is useful in one respect: when a technology is perceived as powerful enough to affect national security, public safety, or the structure of society, technical readiness alone does not determine the pace of adoption. Governance can become part of the innovation cycle.

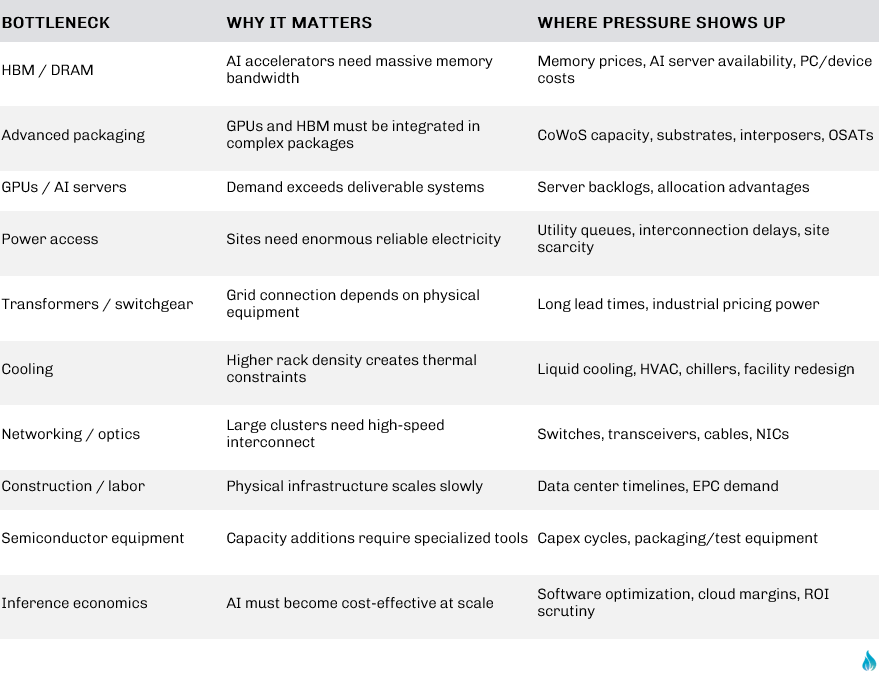

The second constraint is physical infrastructure. AI is increasingly moving beyond the digital economy and into the physical economy, where bottlenecks are more visible. Data centers need power, land, water, cooling, transformers, switchgear, construction labor, electrical contractors, permitting, and grid interconnection. The International Energy Agency estimates that global data center electricity consumption could more than double by 2030, with AI as a major driver. Wood Mackenzie estimates that the U.S. data center electrical equipment market could grow from about $20 billion in 2026 to $65 billion by 2030, with data centers potentially becoming a much larger share of total demand for transformers, switchgear, and power distribution equipment.

This creates a classic economic issue known as crowding out. In its traditional form, crowding out refers to one source of demand absorbing scarce capital or resources, making them more expensive or less available for others. In today’s AI cycle, the crowding out is not only financial. It is physical. AI data centers can absorb scarce electricians, mechanical contractors, engineers, transformers, power equipment, grid capacity, and construction capacity. That can lengthen timelines and raise costs for other projects competing for the same labor and equipment. This does not mean AI is the only reason construction, utility, or equipment costs are rising. Interest rates, insurance, tariffs, permitting, and labor demographics also matter. But in markets with heavy data center, semiconductor, and power infrastructure development, AI can become an additional source of bottleneck inflation.

Memory is one of the clearest examples. AI data centers require large amounts of specialized enterprise memory and storage. As suppliers dedicate more capacity to these higher-value AI and server applications, supply can tighten for more traditional consumer products such as PCs, smartphones, tablets, and gaming devices. TrendForce recently noted that AI server demand and capacity constraints are helping push memory contract prices higher, while some suppliers have reduced emphasis on lower-margin consumer memory products. This pressure is beginning to show up in consumer technology pricing. Recent reporting has noted that Apple and Microsoft have raised prices on certain devices and hardware as memory and component costs increased, with AI-related demand cited as one contributor. In that sense, AI is no longer only influencing semiconductor equity returns. It is beginning to affect the replacement cost of everyday technology products.

The third constraint is economics. AI usage is growing quickly, but many applications remain expensive to run. Training frontier models requires enormous upfront investment, while ongoing usage costs rise as users generate more queries, images, video, code, and automated workflows. The industry often refers to this as the challenge of token economics: the revenue earned per unit of usage must eventually exceed the cost of serving that usage, including compute, memory, energy, networking, and depreciation. If model capability improves but each incremental customer interaction remains expensive, the business model can remain capital intensive even when demand is strong.

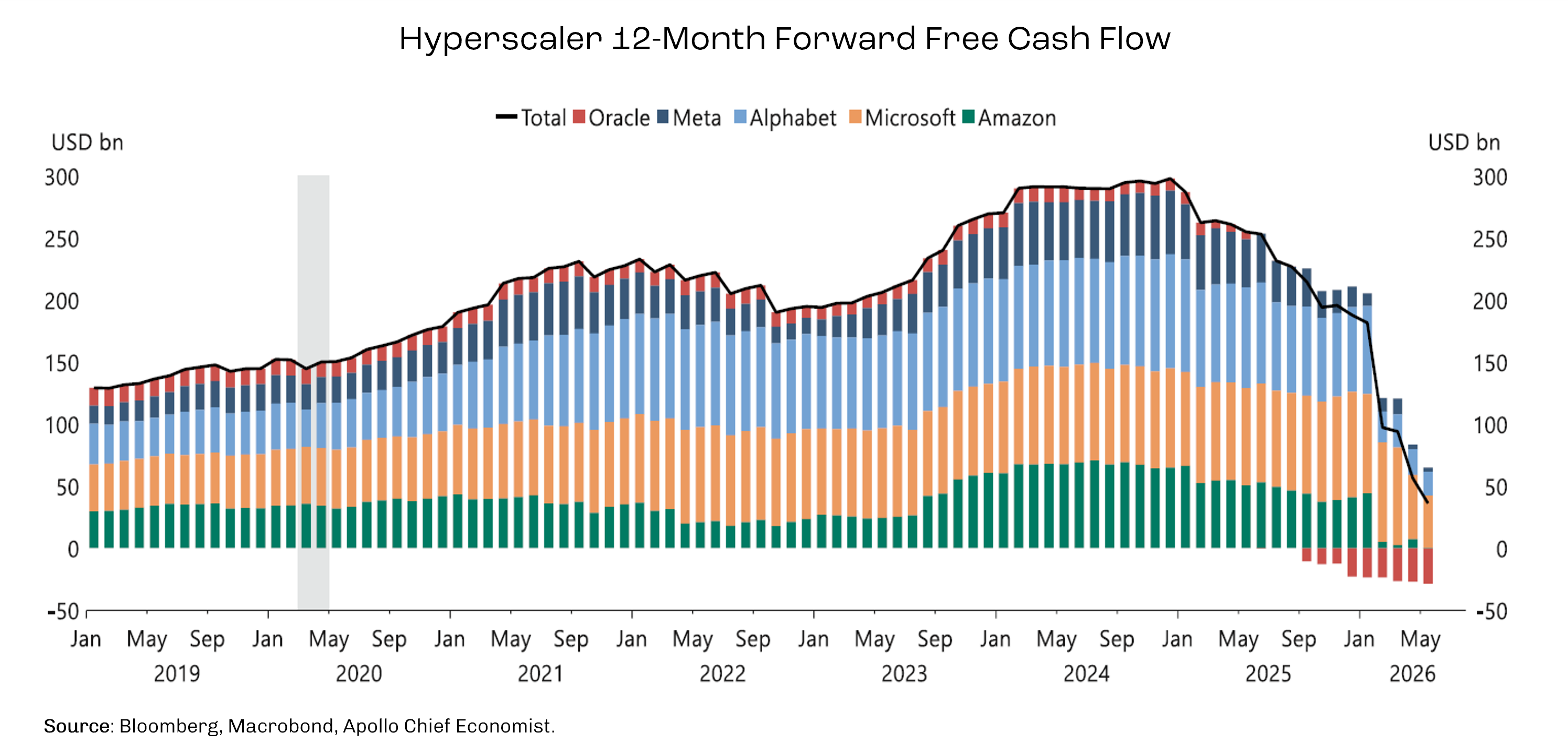

Hyperscaler free cash flow is therefore an important pressure point, and there are signs it is already waning. Apollo’s Chief Economist recently highlighted that 12-month forward free cash flow for the major hyperscalers has declined sharply from its 2024 peak, as AI-related capital spending has accelerated. The largest cloud and platform companies still have the balance sheets to fund the buildout, but even they face tradeoffs. More spending on data centers, chips, networking, and power infrastructure can reduce near-term free cash flow, increase depreciation, and potentially require more debt issuance, leasing structures, or capital partnerships. That does not make the spending wrong. Railroads, telecom networks, cloud computing, and semiconductor fabs all required major upfront investment. But it does raise the hurdle for future returns. At some point, investors will ask whether AI capex is creating economic value in proportion to the capital being deployed.

Enterprise adoption is another reason the path may be uneven. Many companies are experimenting aggressively with AI, but broad integration into workflows, compliance systems, customer service, software development, and internal decision-making is not instantaneous. Large enterprises move slowly when technology touches regulated data, cybersecurity, legal liability, customer privacy, and mission-critical operations. Pilot programs can be exciting, but enterprise-wide transformation requires training, process redesign, procurement approval, vendor governance, and measurable productivity gains. This is why a technology can be revolutionary and still take years to appear fully in productivity statistics.

None of these challenges suggest that AI’s long-term importance has peaked. In fact, they may indicate the opposite: AI is becoming important enough to affect the real economy. The investment cycle is no longer only about software capability or investor imagination. It is increasingly about power availability, supply chains, regulation, financing, enterprise adoption, and return on capital. Technologies that matter eventually collide with constraints, and the next stage of the AI cycle will likely be defined by how well companies, regulators, utilities, and capital markets manage those constraints.

Our view remains that AI has more room to run, but the easy phase of the narrative may be behind us. The market already understands that AI could be transformative. The more important question now is who earns attractive returns after accounting for the cost of infrastructure, energy, capital, regulation, and competition. That does not make us pessimistic on AI. It makes us more selective in how we think about the opportunity.

From a traditional economic perspective, our view remains constructive. The economy is still resilient, the labor market is stable, corporate profits are strong, and AI investment continues to provide meaningful support. Lower oil prices, World Cup activity, and fiscal support may also create room for upside surprises in the near term.

That said, we have grown more attentive to the factors that could destabilize this resilience. Inflation remains uneven, the Fed’s communication framework is changing, political uncertainty is likely to rise, and AI-related expectations are high. In this environment, understanding what is inside a portfolio matters as much as the headline allocation. Broad market exposure may carry more concentration, more AI sensitivity, and more index-construction complexity than many investors realize.

The current environment does not call for abandoning long-term discipline. It calls for humility, selectivity, and a clear understanding of the risks being taken. As always, our focus remains on building resilient portfolios that can participate in growth while recognizing that markets rarely move in straight lines.

Michael is the founder of Fire Capital Management.

.png)