Written by

Ryan Fujioka

Written by

Ryan Fujioka

Published on

March 12, 2026

Category

Investment Insights

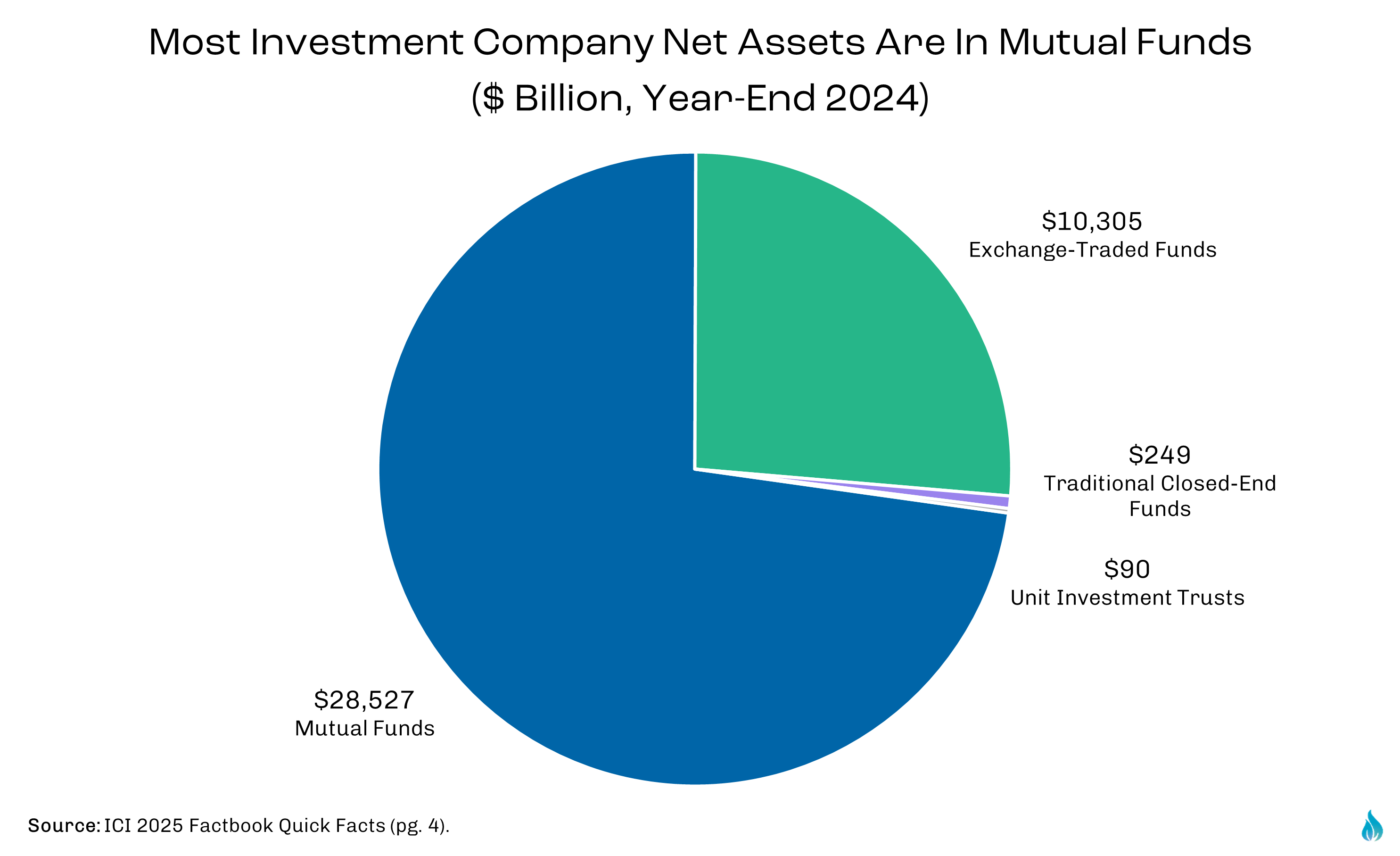

Every investment strategy requires a vehicle. Sometimes called a wrapper or shell, the vehicle provides the legal and operational structure that contains the portfolio of securities in which investors participate. Mutual funds and exchange-traded funds (ETFs) represent the most prominent publicly available pooled investment vehicles in the asset management industry today. Of the $39.2 trillion held in US-registered investment companies as of year-end 2024, mutual funds and ETFs collectively accounted for approximately 99% of those assets1.

Mutual funds and ETFs are similar in concept. Both are publicly registered, professionally managed pooled investment vehicles that offer investors diversified exposure to a wide range of securities. Despite these similarities, several structural differences create important implications for both investors and asset managers. Chief among these differences are tax treatment, trading mechanics, and fee considerations, which have contributed to the evolution of the industry and will continue to shape the outlook going forward.

Tax considerations are arguably the most important difference given their impact from a long-term investment perspective. The key tax distinction between mutual funds and ETFs lies in how investors enter and exit each vehicle. Mutual fund shares are created and redeemed by the fund itself rather than being traded between investors on an exchange. Investors typically place orders through intermediaries, which are ultimately processed with the fund through issuance or redemption of shares at the fund’s end-of-day net asset value (NAV). When investors redeem shares, the fund must typically raise cash to meet those redemptions by selling securities from the portfolio. If those securities have appreciated in value, the sale realizes capital gains within the portfolio. Under US tax rules, mutual funds must distribute realized capital gains to shareholders at least annually, meaning investors may incur a tax liability even if they have not sold any shares themselves.

ETFs operate differently. Because most ETF trading occurs between investors on an exchange rather than directly with the fund, investor activity does not typically force the fund to sell securities in the same way it can with mutual funds. This is possible because ETF shares are created and redeemed through an in-kind process in which large financial institutions known as authorized participants (APs) exchange baskets of securities for ETF shares rather than transacting in cash. During redemptions, this mechanism allows the ETF issuer to transfer low-basis securities (those with large unrealized capital gains) out of the portfolio without selling them. In practice, the redemption basket does not always perfectly mirror the fund’s holdings, and the weights of individual securities may differ slightly from those in the portfolio. This flexibility allows the issuer to include proportionally more securities with the largest embedded gains in the redemption basket, allowing them to leave the portfolio in kind without realizing capital gains, which is good news for investors seeking lower taxes.

In mutual funds, investors transact in specific share classes which generally determine fee structures and require different investment minimums. Fees can be either a) one-time or b) ongoing. Ongoing fees generally consist of three components: the management fee paid to the investment adviser, distribution and service fees (formally 12b-1 fees, also known as the distribution layer), and other operating expenses (related to administration, custody, accounting, and shareholder reporting). Aside from minimum investment requirements, the key consideration for investors in choosing a share class is their intended investment time horizon, which determines the optimal fee structure associated with different types of share classes. At Fire Capital, we primarily invest in what are known as institutional or no-load shares due to our ability to leverage scale and meet minimum investment thresholds. This share class does not charge sales loads and provides the added benefit of having a lower ongoing fee, mostly due to omission of the distribution layer.

ETFs generally do not offer multiple share classes, relieving investors of both the burden of choice regarding mutual fund share classes and their associated minimum investment thresholds. Rather than being built into different fee structures, their cost is decided entirely by the expense ratio and trading conditions on the secondary market (the exchange), which is expressed through the bid-ask spread. Spreads are determined mostly by the liquidity and volatility of both the fund and the fund’s underlying securities, as well as the level of competition among market makers and even time-of-day considerations. While ETF liquidity is often reflected in the fund’s secondary-market trading volume, a low-volume fund can still be highly liquid since liquidity ultimately depends on the underlying basket of securities.

ETFs can be bought and sold throughout market hours, similar to publicly-traded stocks. This intraday liquidity means the settlement price is known at the time of transaction and investors can typically redeploy the liquidated assets quickly. Mutual funds differ in that transactions occur once per day at the fund’s end-of-day NAV, meaning orders submitted during market hours are executed only after the market closes and proceeds are generally not available for reinvestment until the next trading day.

Other differences include holdings transparency and the ability of mutual funds to close to new investors. ETFs typically disclose their holdings daily, whereas mutual funds disclose them quarterly. Mutual funds can also close to new investors when asset growth threatens the strategy’s effectiveness, since larger asset bases can make it harder to deploy capital without diluting best ideas or moving market prices. ETFs generally cannot close to new investors in the same way, making capacity constraints more difficult to manage for certain strategies.

Mutual funds have long been the dominant pooled investment vehicle in the US. The first modern mutual funds were introduced in the 1920s within a largely unregulated financial environment. Following the stock market crash of 1929 and the Great Depression, the US government introduced a series of reforms that established the modern regulatory framework for US securities markets and investment funds, culminating in the Investment Company Act of 1940 (often called 40 Act) that continues to govern most mutual funds and ETFs today.

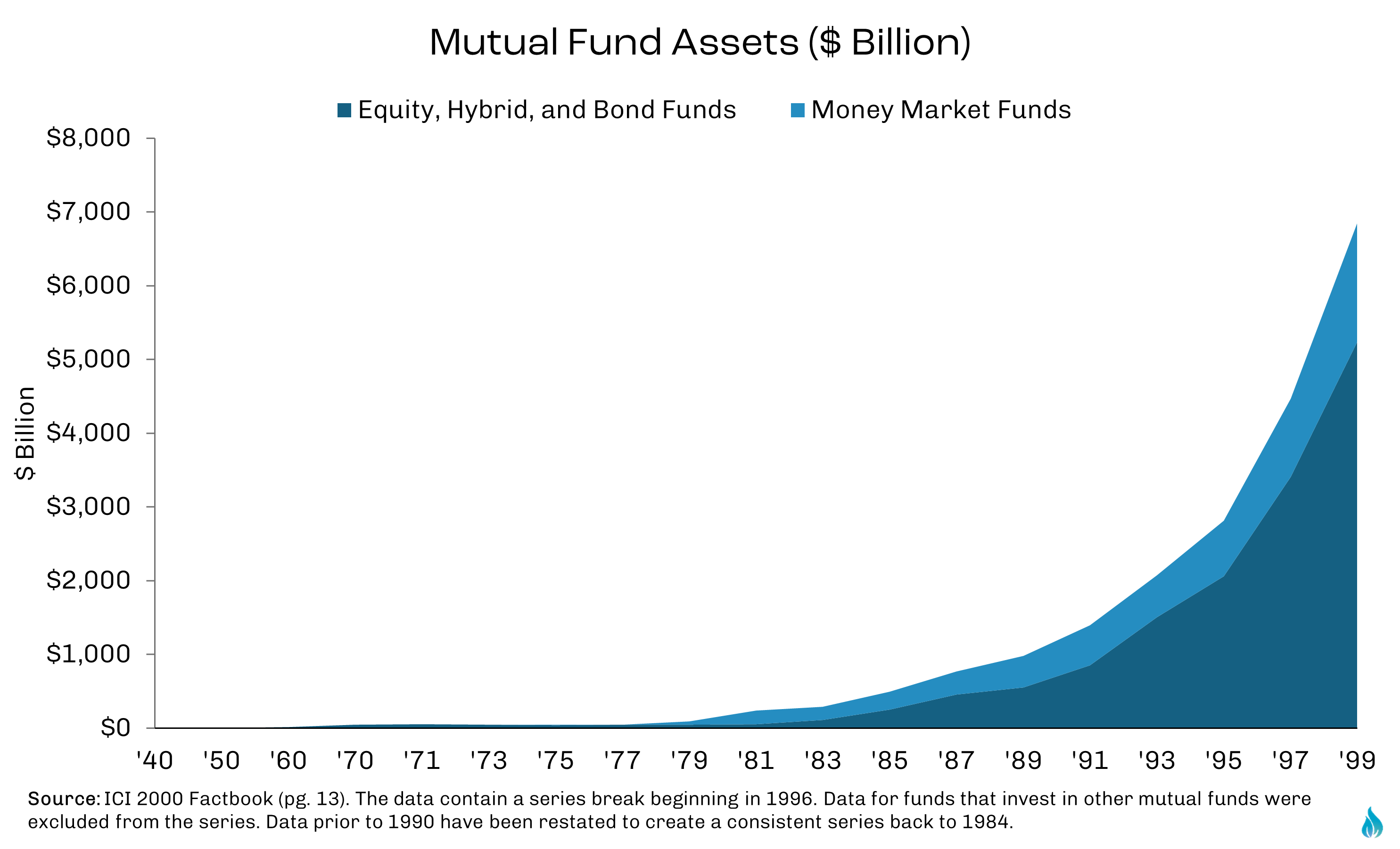

Mutual funds remained a relatively small industry following these reforms, with only about $450 million in assets in 1940. But with the regulatory foundation in place, the industry expanded rapidly over the second half of the century, eventually reaching nearly $7 trillion in assets by 20002. Adjusting for inflation using CPI data, the industry grew more than 1,200x in real terms over the total period. And while it expanded significantly during the post-World War II economic boom, the fastest growth (~25x) occurred between 1980 and 2000 as defined-contribution plans such as 401(k)s became widespread and households increasingly participated in capital markets alongside the long equity bull market of the era.

The rise of passive investing has been one of the primary drivers of the transition toward ETFs. Much of the intellectual foundation for indexing emerged from developments between the 1950s and 1970s, with Harry Markowitz’s work on portfolio diversification, William Sharpe’s capital asset pricing model (CAPM), and Eugene Fama’s efficient market hypothesis playing particularly influential roles. While these ideas are now considered foundational to modern investment management, they were highly revolutionary at the time. The work of Paul Samuelson built on these concepts by advocating for the creation of a fund that simply tracked the S&P 500, an idea that helped inspire Jack Bogle to launch the first retail index fund at Vanguard in 1976.

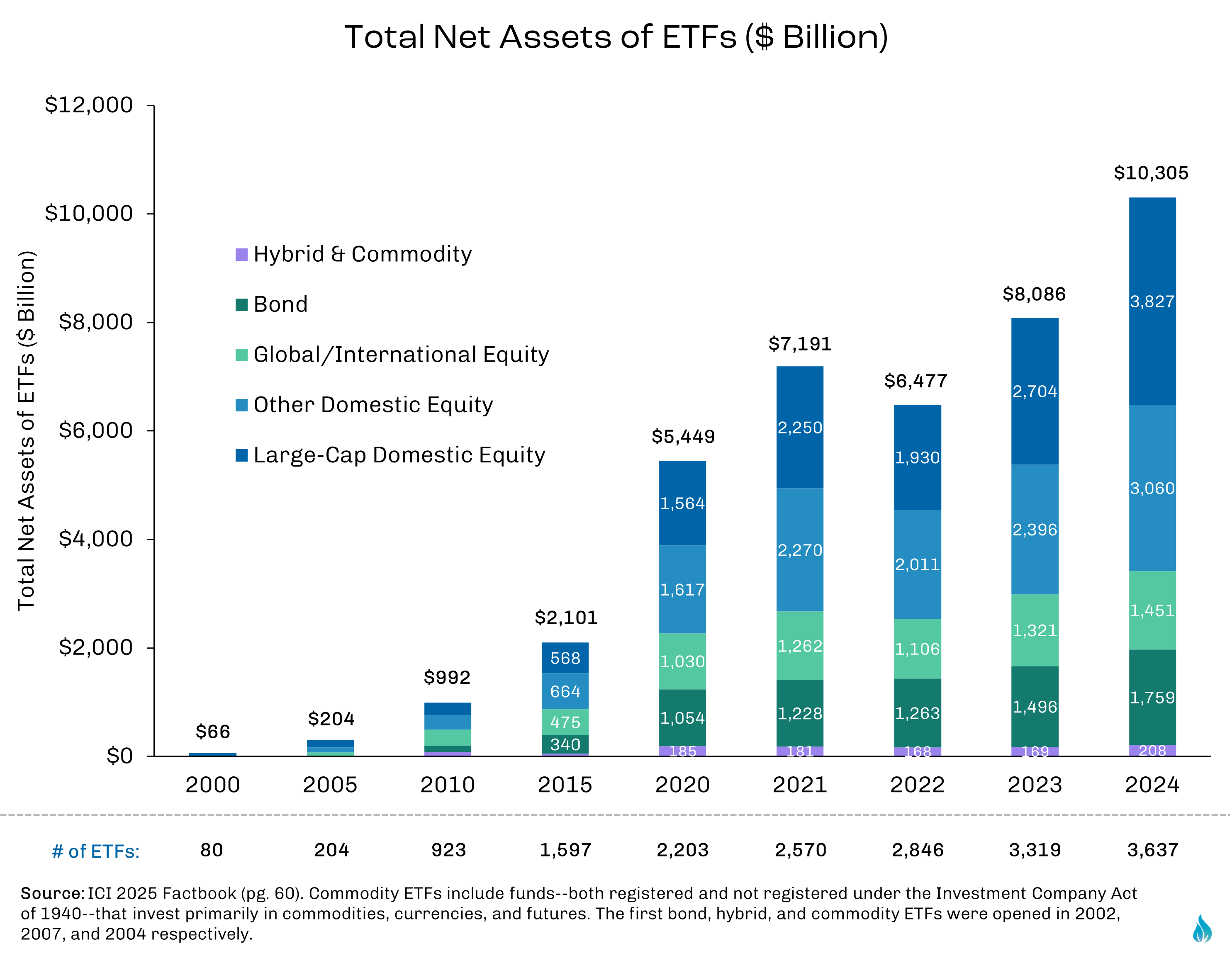

Around the time when the mutual fund industry was peaking, the first modern ETF was introduced by State Street Global Advisors in 1993. ETFs began mostly as index-tracking funds, with roughly $66 billion in assets in 2000 before growing to more than $5 trillion by 2020. Over the period, the ~55x real growth in ETF assets was more than double the comparable peak growth period in mutual funds.

Relative to active strategies, passive strategies eliminate the cost of research and are more operationally efficient due to rules-based (rather than discretionary) portfolio construction, typically resulting in lower trading costs. The influence of passive investing can be seen in the fact that cheap, passive funds have seen the vast majority of inflows over the last 20 years. The cheapest 20% of passive funds saw almost $2.8 trillion of inflows between 2021 and 2024 alone, while all other funds collectively lost $1.2 trillion over the same period3.

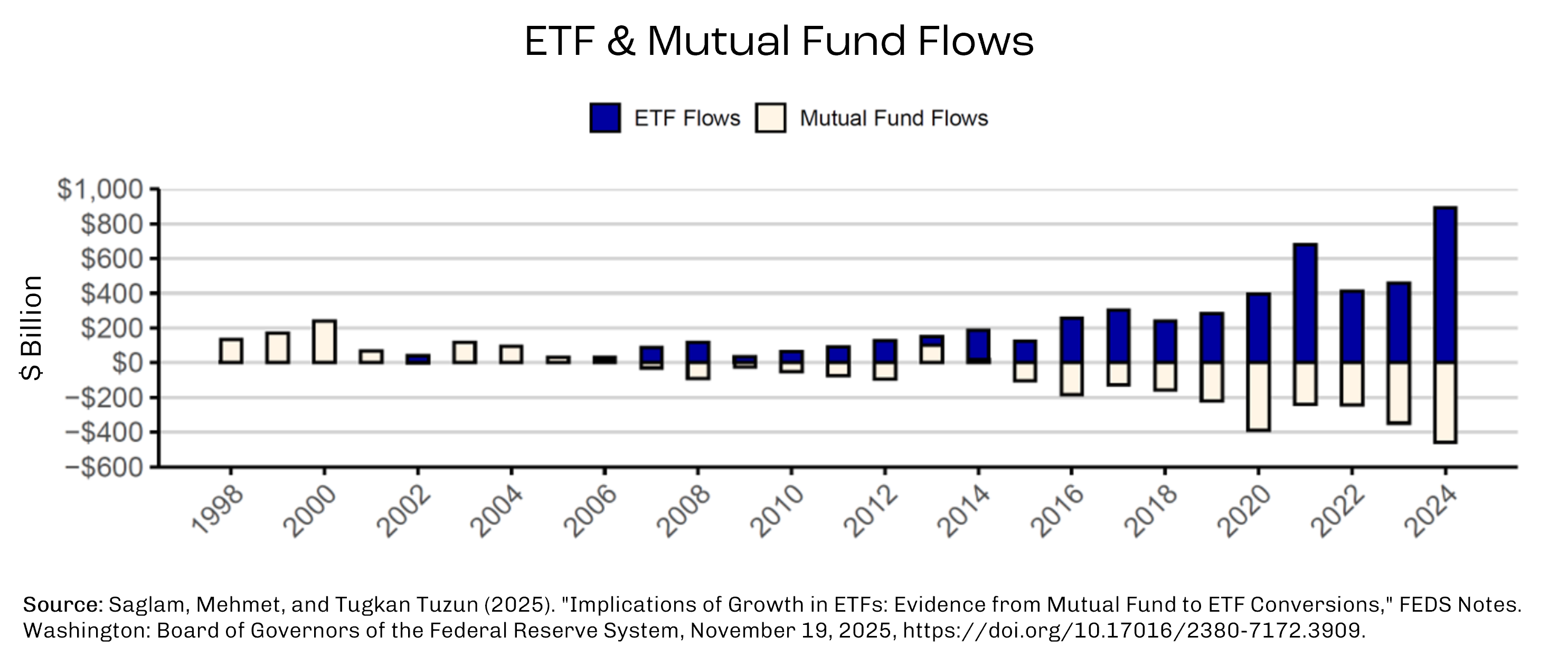

Passive strategies currently make up approximately 90% of ETF assets4, whereas mutual fund assets are mostly active. While both vehicles have seen fee compression over time, ETF fees are roughly half those of mutual funds on an asset-weighted basis, although the difference is less pronounced among passive vehicles3. In addition to the larger influence of cheaper, passive strategies, ETFs also tend to have lower expense ratios due to a combination of lower distribution costs and the structural advantages of their creation and redemption mechanism. These dynamics are reflected in industry flows, with ETF inflows exceeding mutual fund inflows in every year but one since 2006.

Despite the ETF industry’s momentum, mutual funds continue to serve a purpose. They remain deeply embedded in retirement plan channels and some investors prefer transacting at end-of-day NAV rather than dealing with intraday market prices, bid-ask spreads, or limit orders. There are also active managers whose strategies have historically been housed in mutual funds and whose investor base remains comfortable there. In some cases, the nature of the strategy, the underlying securities, or the operational setup may still favor the mutual fund wrapper. That said, the bar is higher than it used to be. Mutual funds must not only justify their fees, but also their structural disadvantages in areas such as taxes, transparency, and trading flexibility. In a market where investors can often access similar exposures through more efficient vehicles, a mutual fund must offer something distinctive to earn a place in the portfolio.

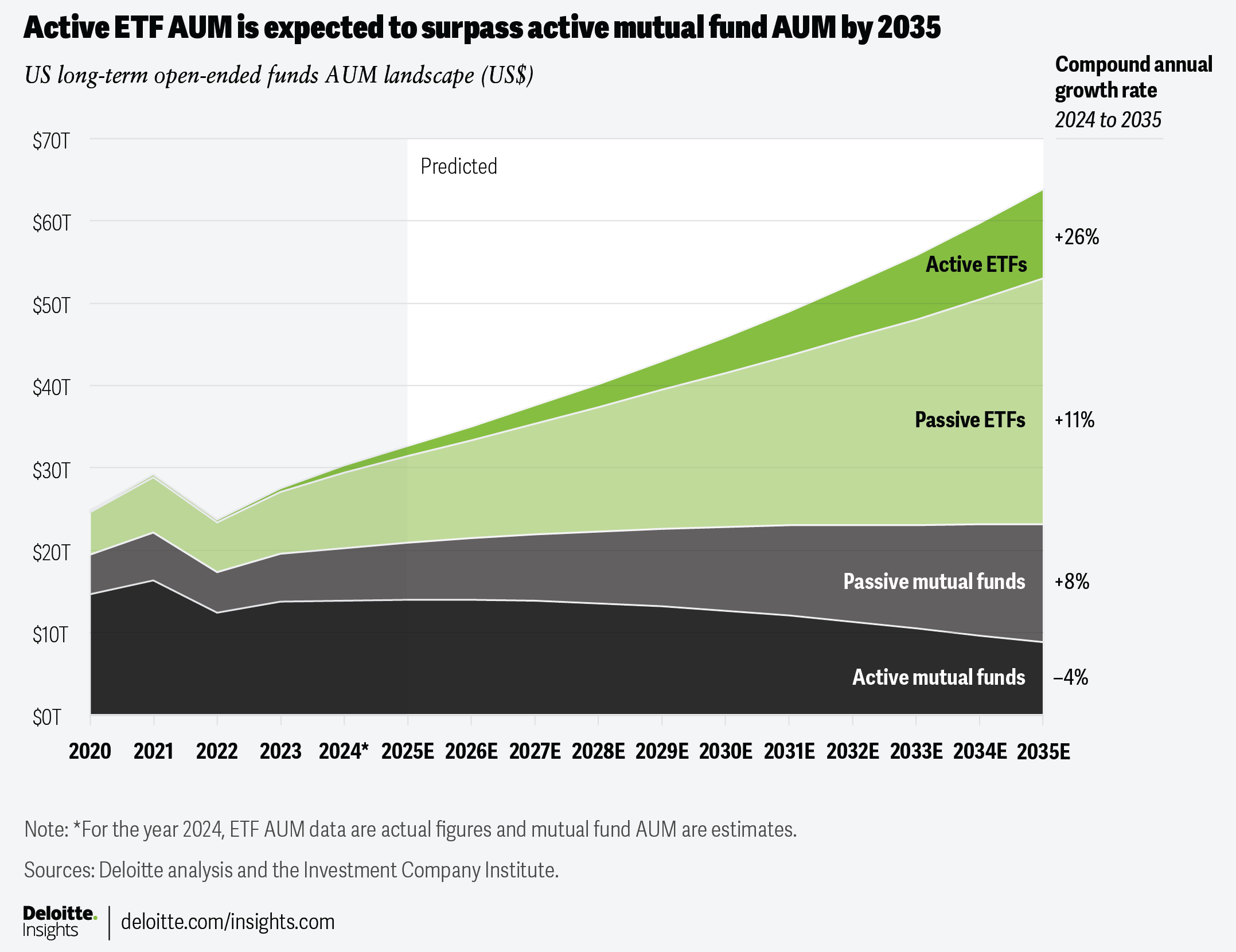

Recent analysis shows continued growth expectations in passive vehicles overall but a strong divergence in where active management will be expressed. While ETFs are expected to continue capturing the lion’s share of investment flows across both active and passive strategies (see below), active ETFs are expected to be the fastest growing segment of the industry at a 26% compound annual growth rate (CAGR) over approximately the next decade.

The outlook for active ETF adoption also reflects a broader shift in how active management is being packaged and distributed. Many active ETFs are not entirely new strategies but rather ETF versions of existing mutual fund strategies, allowing asset managers to deliver familiar investment approaches through a vehicle better aligned with evolving investor preferences and distribution channels. At the same time, the ETF structure has encouraged the development of strategies designed specifically for the exchange-traded format rather than adapted from existing mutual funds. The adoption of the SEC’s Rule 6c-11 (known as the ETF Rule) in 2019 further accelerated this transition by allowing ETFs to launch without case-by-case approval and lowering barriers to entry for issuers.

The fund industry is not moving toward a world where one wrapper eliminates the other, but rather toward one where structure must earn its place alongside strategy. Two strategies with similar mandates can produce meaningfully different investor outcomes once the cumulative effects of fees, taxes, liquidity, and trading behavior are taken into account. ETFs have earned their growth because their structural advantages align well with modern portfolio construction. Mutual funds retain a role that is narrowing and increasingly dependent on cases where the wrapper adds value or is unique to the strategy itself. At Fire Capital, we believe these details matter and collectively explain why we evaluate the investment structure alongside the strategy rather than treating the vehicle as an afterthought.

1 Structures such as collective investment trusts (CITs) and separately managed accounts (SMAs) also represent a meaningful share of professionally managed assets. However, they fall outside the scope of this discussion because they are not both publicly available and pooled investment funds.

2 ICI 2008 Factbook

3 Morningstar 2024 US Fund Fees Study (pg. 16)

4 Saglam, Mehmet, and Tugkan Tuzun (2025). "Implications of Growth in ETFs: Evidence from Mutual Fund to ETF Conversions," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, November 19, 2025, https://doi.org/10.17016/2380-7172.3909.

.png)