Written by

Michael J. Firestone, CFA

Written by

Michael J. Firestone, CFA

Published on

April 9, 2026

Category

Market Trends & Commentary

Investor sentiment has become increasingly shaped by a wide range of potential downside scenarios, many of which are credible but not yet evident in the current data. While risks tied to geopolitical tensions, inflation, artificial intelligence, and private credit are receiving significant attention, much of this concern reflects what could happen rather than what is happening today.

At the same time, the underlying data continues to point to an economy and market backdrop that are more resilient than expected. Strong corporate earnings, improving valuations, a stabilizing labor market, and ongoing fiscal support suggest that the foundation entering 2026 remains intact. If some of the more feared outcomes fail to materialize, the setup for markets in the second half of the year could be more constructive than currently perceived.

1. Key Risks Remain Real and Could Still Derail the Outlook

Geopolitical conflict in Iran, stress within private credit markets, and the pace of AI-driven job disruption all represent credible risks. If these dynamics worsen, they could pressure economic growth and tighten financial conditions more meaningfully than currently reflected in markets.

2. Several Core Conditions Have Improved Relative to Expectations

Despite elevated uncertainty, a number of important factors have developed more positively than expected entering the year. Corporate profitability has improved beyond expectations, valuations have improved, the labor market has green shoots, and policy dynamics have become more supportive in the near term.

3. Markets Are Behaving Consistently With Historical Patterns

Periods of uncertainty, particularly around geopolitical events and political cycles, often lead to short-term volatility without lasting economic damage. Current market behavior, including early-year weakness and sentiment-driven caution, is broadly consistent with historical patterns.

4. The Foundation of the Economy Remains Intact

The global economy entered the year with solid momentum, supported by resilient consumers, strong corporate fundamentals, and ongoing capital flows into U.S. assets. This foundation continues to provide stability despite heightened uncertainty.

5. The Setup Could Be Supportive if Worst-Case Scenarios Do Not Materialize

If some of the more widely discussed downside risks fail to develop, the combination of improving fundamentals, policy support, and normalized valuations could create a favorable environment for markets in the second half of the year.

We entered 2026 from a position of strength, both in the global economy and in portfolio construction. While risks remain elevated and are being closely monitored, current conditions do not yet warrant a shift to a more defensive posture.

The current market environment is defined less by what is happening today and more by what could happen next. Headlines have increasingly focused on a range of downside scenarios, and importantly, many of them are not without merit.

There are credible paths where higher energy prices, driven by ongoing geopolitical tensions, could remain elevated for longer than expected. In that scenario, inflation could reaccelerate, forcing the Federal Reserve to delay or even reverse its expected path toward rate cuts. History has shown that sustained oil-driven inflation shocks can slow economic activity and, in some cases, contribute to recessionary outcomes.

At the same time, the pace of innovation in artificial intelligence introduces a different kind of uncertainty. While the long-term benefits are widely recognized, the near-term labor implications remain unclear. Recent announcements, including Oracle’s plan to reduce its workforce by more than 30,000 employees, highlight the possibility that technological adoption could impact employment more quickly than anticipated.

Financial markets also face evolving risks beneath the surface. The rapid growth of private credit has filled a meaningful gap left by post-Global Financial Crisis banking regulations, particularly in financing small and mid-sized businesses. However, recent developments, including redemption pressures and gating across certain funds, have raised questions about liquidity and valuation within the space. Large platforms such as Apollo, Blackstone, BlackRock, and Blue Owl have become central to this ecosystem, and any signs of stress could have broader implications for financial conditions.

These are not risks we take lightly. They represent the types of scenarios that warrant close attention, particularly because the most disruptive outcomes are often those not fully appreciated ahead of time. And yet, as we worked through these points, something became clear. Much of what we were writing sounded familiar. Not because it was incorrect, but because it closely resembled what is already being said across financial media and social platforms. In many cases, these risks are well understood, widely discussed, and increasingly reflected in sentiment.

At the same time, several important dynamics have received far less attention. The global economy entered the year with strong momentum, supported by resilient consumer activity, solid corporate earnings, and improving policy dynamics. It is also worth noting that the path of markets over the past several years has been relatively smooth by historical standards.

Periods of relative stability can create their own form of unease, as investors begin to anticipate the next disruption simply because one has not occurred recently. In that sense, some of the current caution may reflect positioning and sentiment as much as underlying economic reality.

Ultimately, the tension between what could happen and what is happening is central to today’s market environment. Our goal in this commentary is not to ignore the risks, but to balance them with the realities unfolding today. In doing so, we believe the setup for markets may be more constructive than widely perceived, particularly if some of the more feared outcomes fail to materialize in the months ahead.

While much of the current narrative is focused on uncertain forward-looking risks, the data today continues to reflect an economy that is holding up better than expected across several key dimensions.

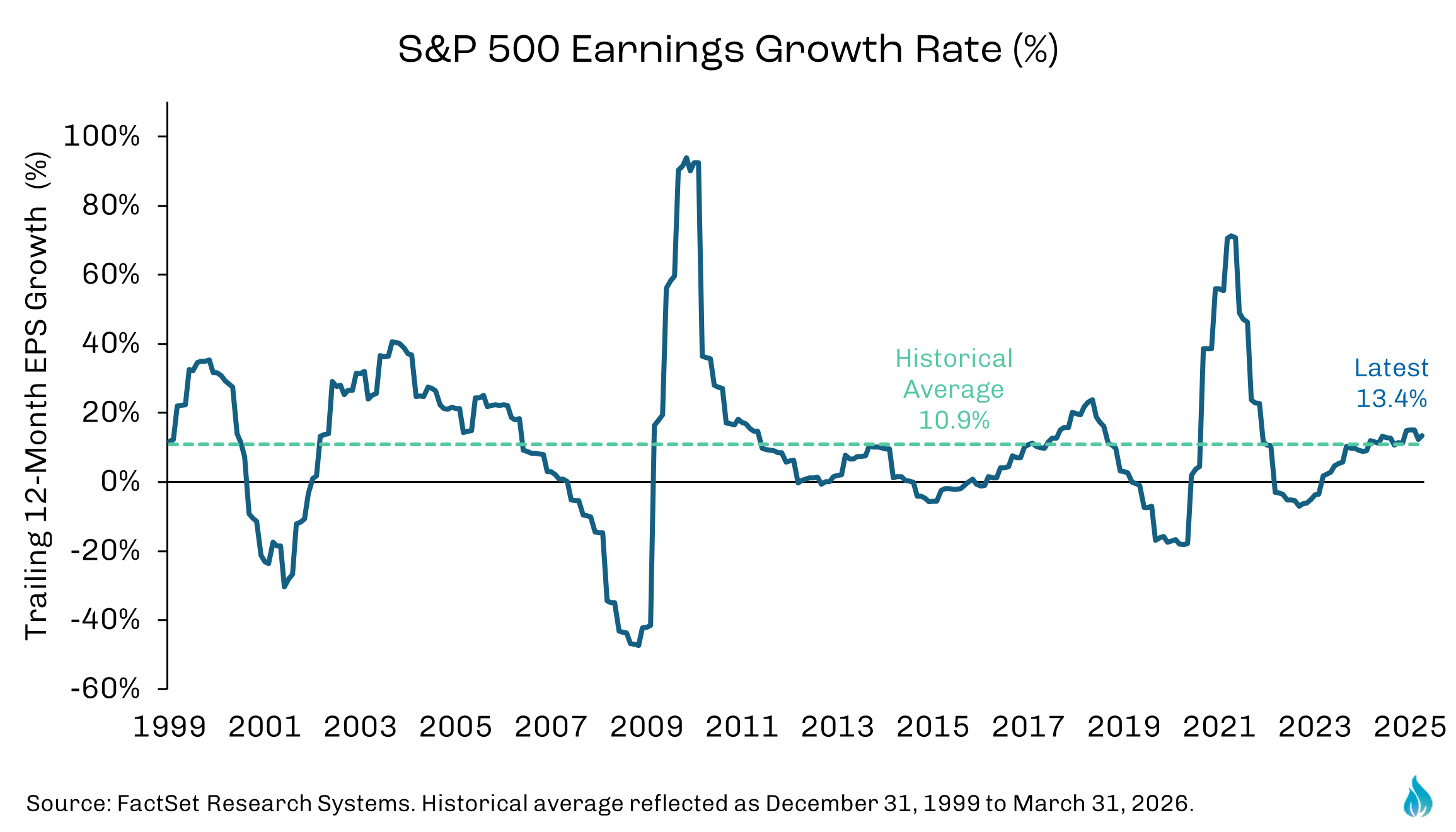

The S&P 500 is on pace for what could be a sixth consecutive quarter of double-digit earnings growth, with first quarter earnings expected to increase approximately 13%-15% year over year. Importantly, estimates have been revised modestly higher over the course of the quarter, which runs counter to the typical pattern where estimates move lower as reporting periods approach.

Revenue growth has also remained strong, with first quarter revenues expected to grow nearly 10% year over year, marking the highest level since 2022. All eleven sectors are projected to deliver positive revenue growth, reinforcing the idea that demand remains broadly supported across the economy. At the same time, margins have held firm, with net profit margins expected to come in above both year ago levels and longer term averages.

Forward expectations further support this narrative. Consensus estimates call for full-year 2026 earnings growth of approximately 17%–18%, with quarterly growth expected to accelerate into the 19%–21% range.

Valuations were a key concern entering the year, particularly given the elevated multiples driven by strong market performance over the last 3 years. With corporate earnings rising and markets fading to start the year, this dynamic has improved in a more constructive way than many expected.

The forward 12-month P/E ratio for the S&P 500 has declined to approximately 19.8x, down from roughly 22x at the end of 2025. While still modestly above the 10-year average, valuations are now in line with the 5-year average, suggesting that much of the prior premium has normalized.

What is particularly notable is how this adjustment has occurred. Since the start of the year, forward earnings estimates have increased by more than 7%, while index prices have declined modestly. If some of the war driven overhang lifts, the current environment reflects a healthy reset, one where earnings growth is doing the work in bringing valuations back toward more sustainable levels.

Taken together, the combination of strong earnings growth, broad based revenue expansion, stable margins, and improving asset valuations lead to an important point. While uncertainty has increased, corporate fundamentals remain solid and, in several cases, better than expected.

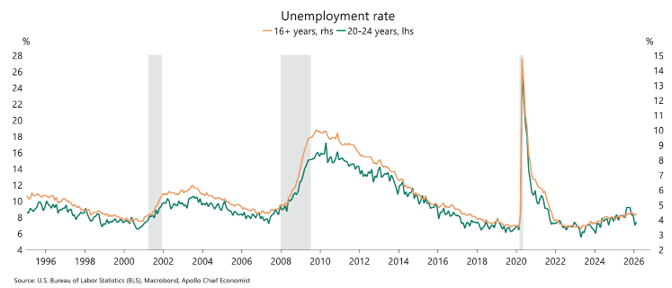

One of our primary concerns entering 2026 was that a cooling labor market could transition into something more pronounced. The “no hire, low fire” environment that defined much of 2025 was viewed as a late-cycle signal and, in some cases, expected to deteriorate further amid concerns around artificial intelligence and slowing economic momentum.

Recent data has been more encouraging. According to the Bureau of Labor Statistics, non-farm payrolls increased by 178,000 in March, well above expectations and a meaningful improvement from prior months. The payrolls diffusion index also moved higher, indicating broader participation in hiring across industries and suggesting that labor demand remains more resilient than feared.

At the same time, one of the more widely discussed risks entering the year was the potential for artificial intelligence to begin displacing workers, particularly younger and entry-level employees. However, the data to date does not show evidence of this materializing in a meaningful way.

As shown in the chart above, the unemployment rate for younger workers has largely moved in line with the broader labor market, with no clear signs of disproportionate weakness. If AI-driven displacement were accelerating, it would likely appear first in this segment. Instead, the data suggests the labor market remains stable rather than structurally disrupted. This is not to suggest there has been no impact or that future challenges will not emerge, but the data does not support the view that displacement is already widespread.

While the pace of job growth has moderated, it remains near levels consistent with labor market stability. Goldman Sachs estimates that the underlying pace of job growth is roughly in line with the breakeven level needed to keep the unemployment rate stable, as expressed in the latest unemployment rate reading, which declined to 4.26%. In combination, the data points to positive improvement in the labor market relative to expectations entering the year.

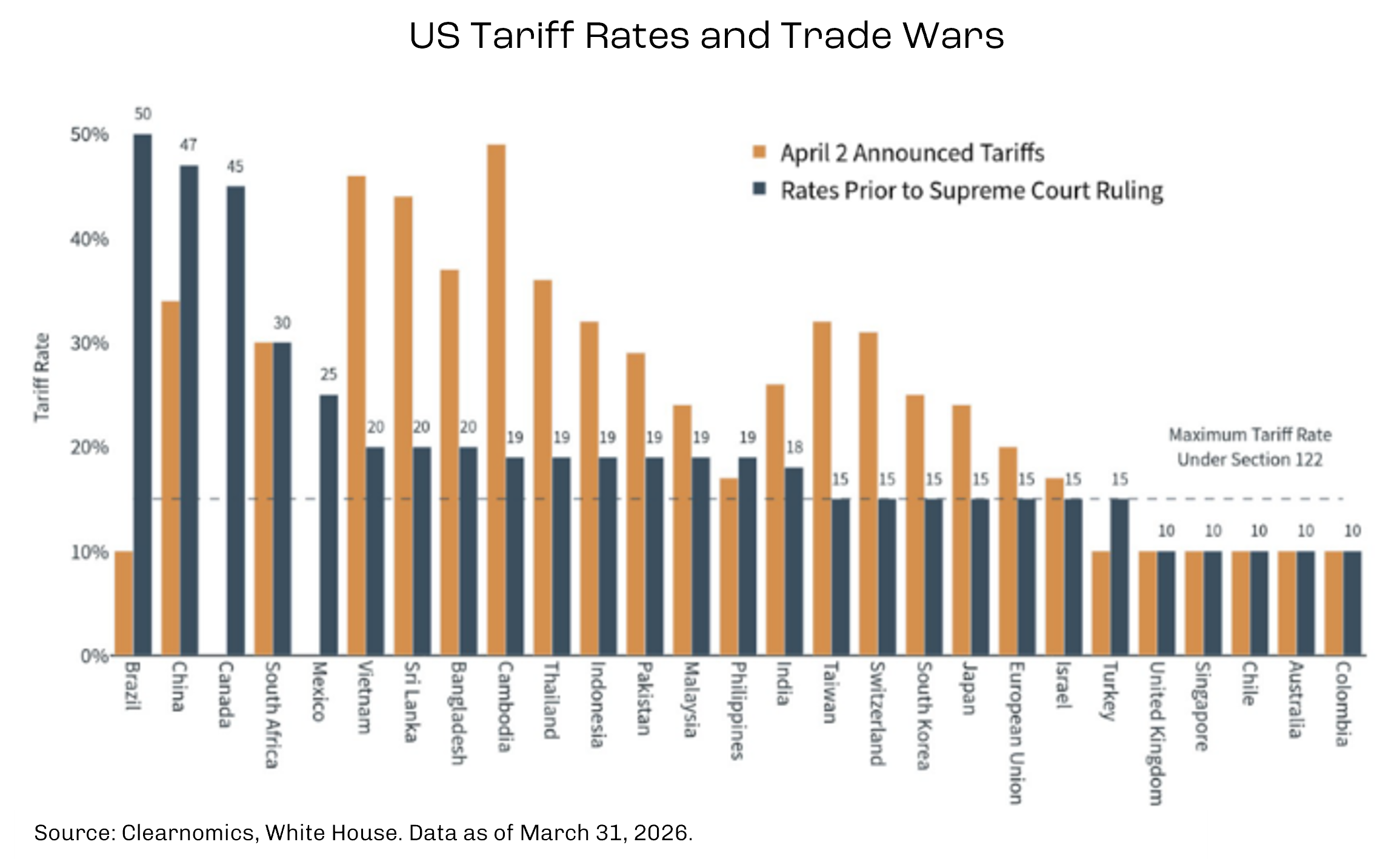

Heading into 2026, tariffs were widely viewed as a drag on economic growth and a potential source of upward inflation pressure. However, much of that impact had already been absorbed by markets, with businesses and investors adjusting expectations accordingly.

One of the most consequential policy developments in the first quarter was the Supreme Court ruling on tariffs. In a 6–3 decision, the Court determined that broad tariffs imposed under the International Emergency Economic Powers Act were unlawful, placing more than $175 billion in tariff collections at risk, according to the Penn Wharton Budget Model.

Despite the ruling, the Trump administration quickly implemented a temporary global import tariff under Section 122 of the Trade Act of 1974, initially at 10%, with the authority to increase rates up to 15%. At the same time, new Section 301 investigations were launched, signaling an intent to maintain tariff pressure through alternative channels. In effect, the legal framework has changed, but the broader policy direction remains intact.

That said, the near-term impact has been more constructive. Effective tariff rates are now lower than they were prior to the ruling, easing cost pressures on businesses and reducing the immediate pass-through to inflation.

An often-overlooked consequence of the ruling is the potential for tariff refunds to support corporate balance sheets. Bloomberg Law analysis suggests companies may be eligible to recover previously paid tariffs, potentially with interest. While timing remains uncertain, these refunds represent a potential injection of liquidity that could support reinvestment, debt reduction, or shareholder returns.

While tariff policy remains fluid, first quarter developments suggest its near-term impact may be less of a headwind than expected. In fact, when considering both lower effective rates and the potential for refunds, tariffs have shifted from a known drag to a more balanced, and in some cases modestly supportive, factor for the economy and corporate sector.

While much of the current narrative is focused on risks to growth and the consumer, the underlying policy and capital backdrop remains more supportive than widely appreciated.

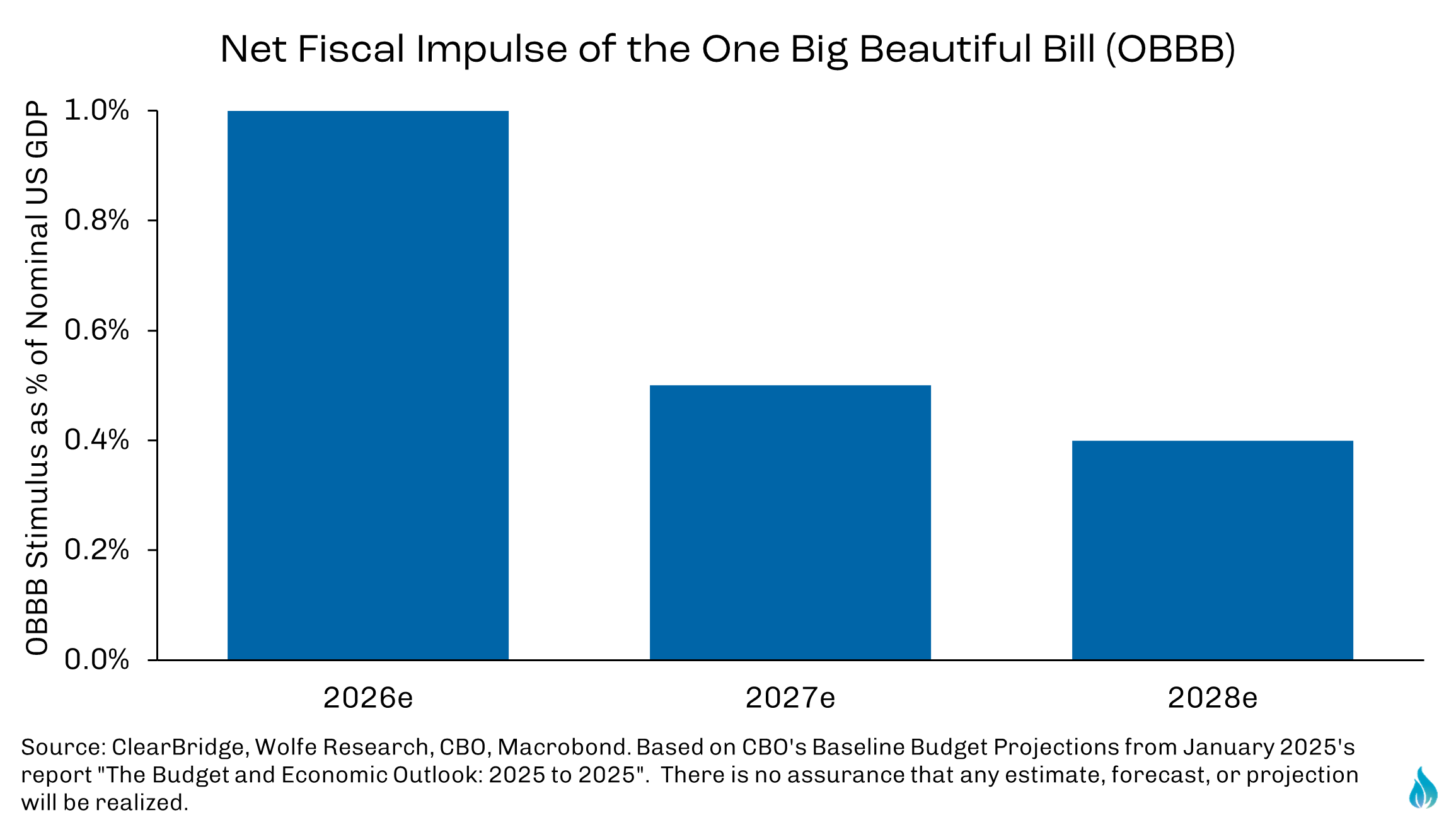

One of the important drivers is tax legislation associated with the One Big Beautiful Bill Act (OBBBA), which is expected to deliver a meaningful fiscal impulse in 2026. As shown in the chart below from ClearBridge, estimates suggest the bill could contribute approximately 1% of GDP in stimulus this year, with support remaining positive, though moderating, in 2027 and 2028.

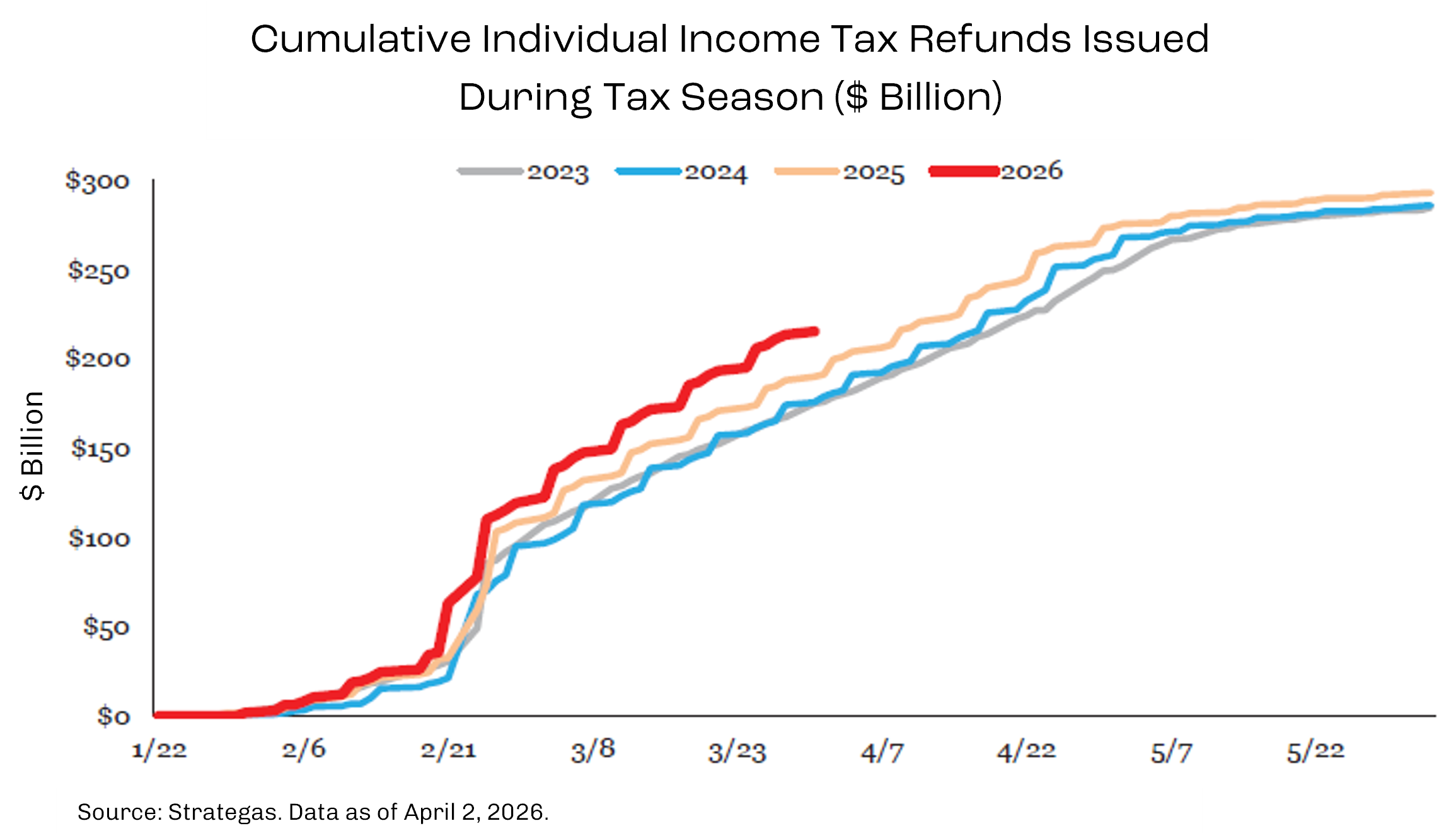

The stimulus is already beginning to show up in real economic activity. As illustrated in the chart below from Strategas, tax refunds have accelerated meaningfully in 2026 compared to prior years, reflecting the impact of recent tax changes.

Tax refunds represent a direct injection of liquidity into both households and businesses. For consumers, this supports near-term spending and financial flexibility. For corporations, provisions such as accelerated depreciation improve cash flow and balance sheet strength. When combined with the potential for tariff refunds, this creates an environment where cash is being returned to the private sector.

This dynamic is also supported by forward-looking indicators. Research from Piper Sandler suggests that improving profitability and business confidence tend to lead labor market strengthening with a lag, reinforcing the idea that policy support is still working its way through the system.

The consumer, often viewed as the most important indicator of the health of the broader economy, has remained more durable than expected. Stable employment conditions and increased liquidity from tax-related policy changes continue to support spending and help buffer against downside risks.

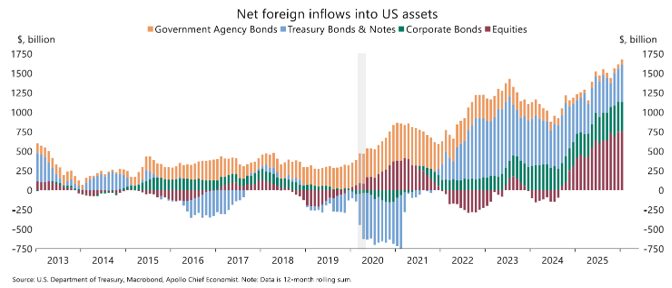

Finally, the idea that global investors are pulling back from U.S. assets is not supported by the data. Apollo’s Chief Economist highlights that net foreign inflows into U.S. assets have strengthened, with sustained demand across Treasuries, corporate bonds, and equities.

Despite elevated geopolitical uncertainty and ongoing policy shifts, the U.S. continues to attract global capital at a high level.

The key takeaway is that these factors point to an environment where policy support, corporate strength, and capital flows are working in the same direction. While risks remain elevated, the data suggests the economy is in a better position than many anticipated entering the year, even as uncertainty has increased.

While uncertainty has dominated headlines in recent months, it is important to recognize that periods like this are not unusual in a historical context. Markets are constantly navigating a wide range of risks, including geopolitical conflict, policy shifts, and economic slowdowns. What often feels unique in the moment tends to follow more familiar patterns when viewed through a longer-term lens.

History does not suggest that uncertainty should be ignored, but it does provide important context for how markets typically respond. In many cases, market behavior during periods of elevated uncertainty reflects anticipation and adjustment rather than lasting impairment. Understanding these patterns can help investors separate short-term noise from longer-term trends.

Periods of heightened uncertainty often feel unique in real time, but history suggests that markets tend to process these events more quickly than expected.

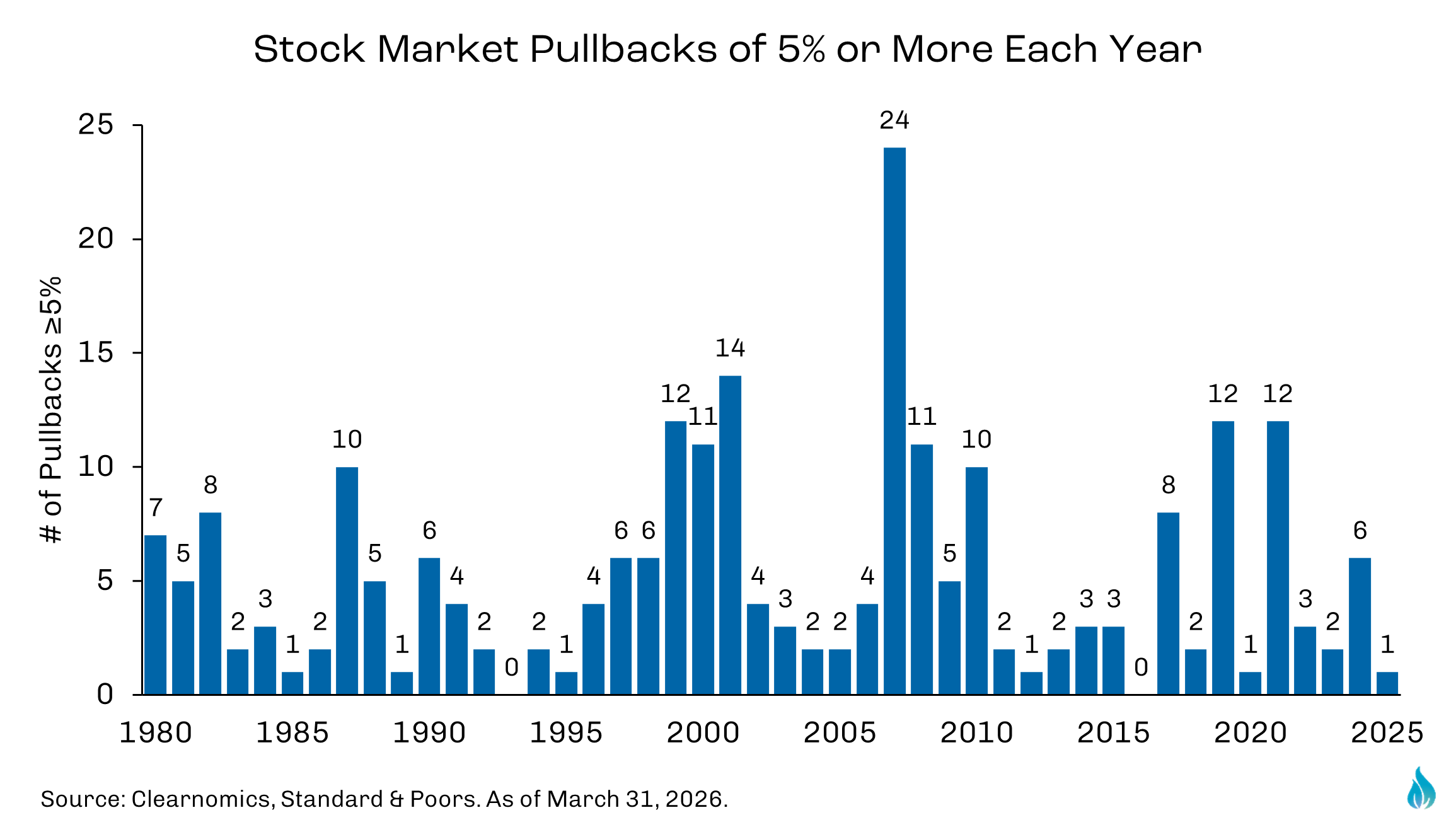

The first quarter is a good example. The S&P 500 declined approximately 4.3%, matching the drawdown experienced in the first quarter of last year. While this has contributed to a more cautious tone, early-year volatility is not uncommon, particularly in environments shaped by elevated uncertainty.

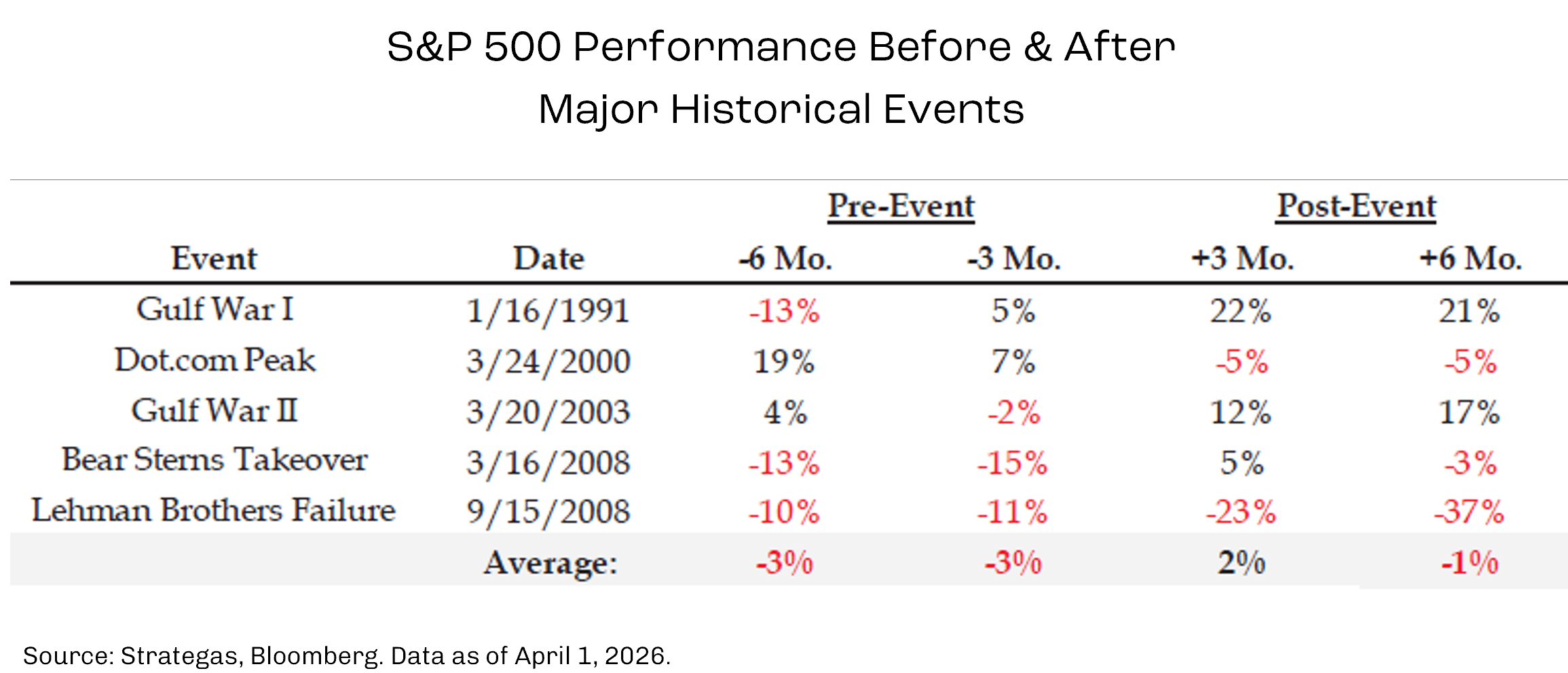

Geopolitical risk remains a central concern. However, as shown in the chart below, market performance around major geopolitical and financial events has historically been mixed, with returns often stabilizing or improving in the months following the initial shock.

This aligns with recent commentary from Fundstrat’s Tom Lee, who noted that across multiple major conflicts, markets tend to bottom within the first 10% of a war's duration. For World War II, that was 5 months. While each situation is unique, the broader takeaway is that markets tend to discount uncertainty rapidly, often before there is clarity on outcomes.

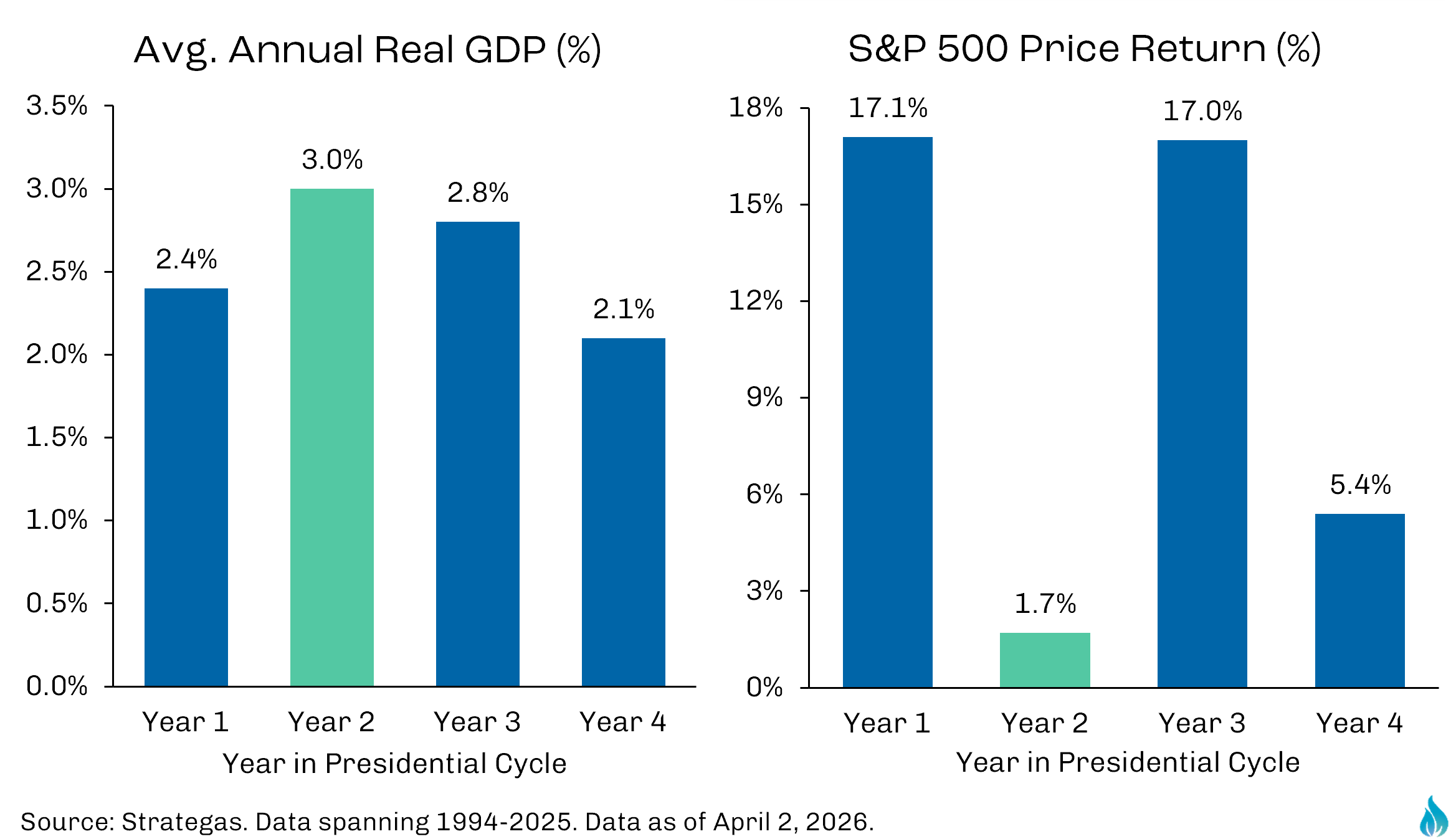

Political and economic cycles provide another example of how market performance can diverge from underlying fundamentals.

As shown in the charts below, economic growth has historically been strongest during midterm election years. Despite this, equity market returns during these same periods have tended to be weaker on average.

This divergence highlights an important point. Markets are forward-looking and often reflect uncertainty ahead of improving economic conditions. In other words, weaker market performance does not necessarily indicate a weakening economy.

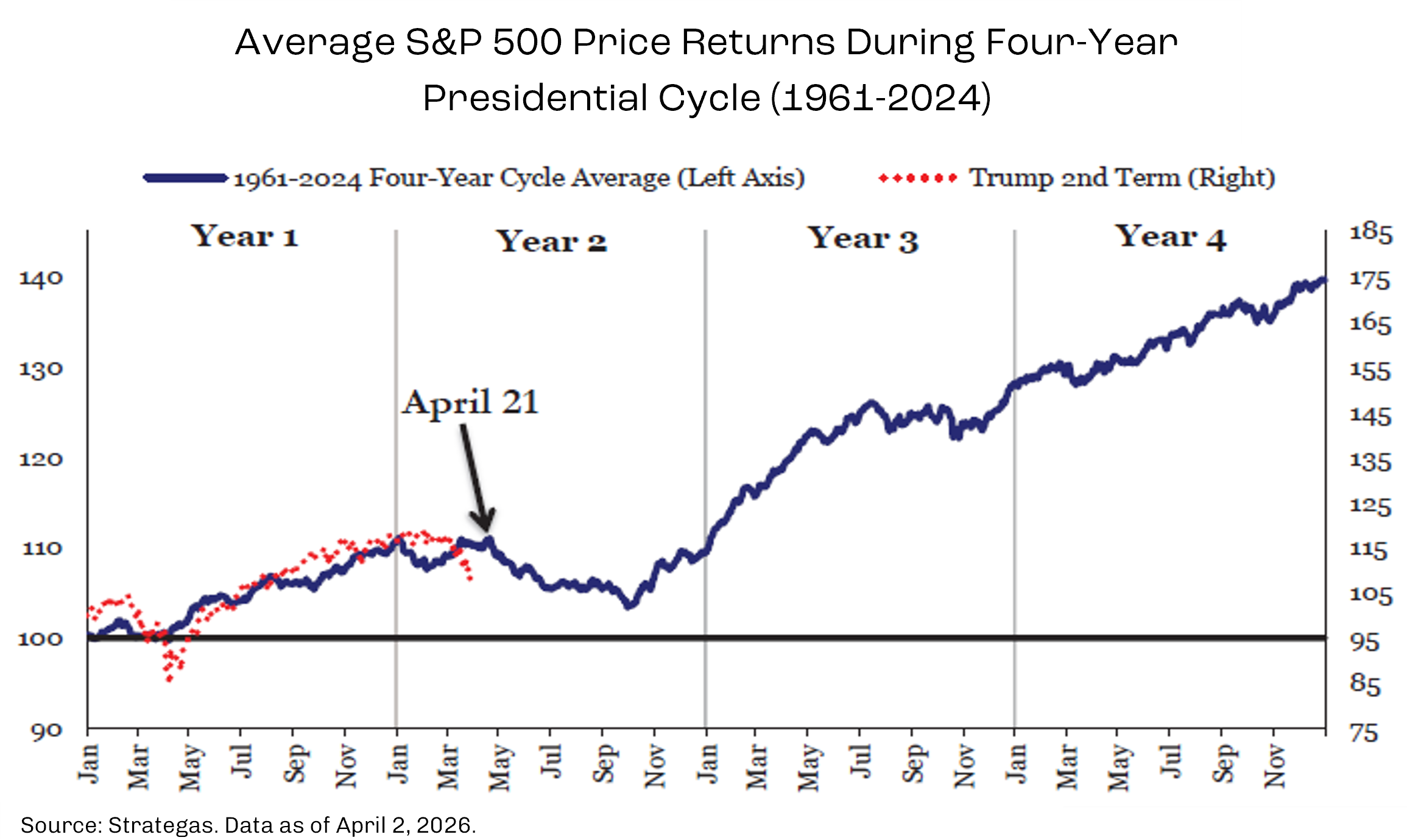

Recent market behavior appears consistent with this pattern. As shown below, the S&P 500’s trajectory in 2026 has closely tracked the historical path of a midterm election year, including a period of early-year volatility followed by stabilization.

Periods of market stress are not only common, but a necessary part of long-term investing.

As shown in the chart below, markets have experienced repeated “panic events” over the past several decades, ranging from geopolitical conflicts to financial crises and policy shocks. While these events have often led to meaningful drawdowns in the short term, they have not prevented the market from compounding over longer time horizons.

This underscores an important reality. Volatility is not an anomaly. It is the cost of participating in long-term market growth.

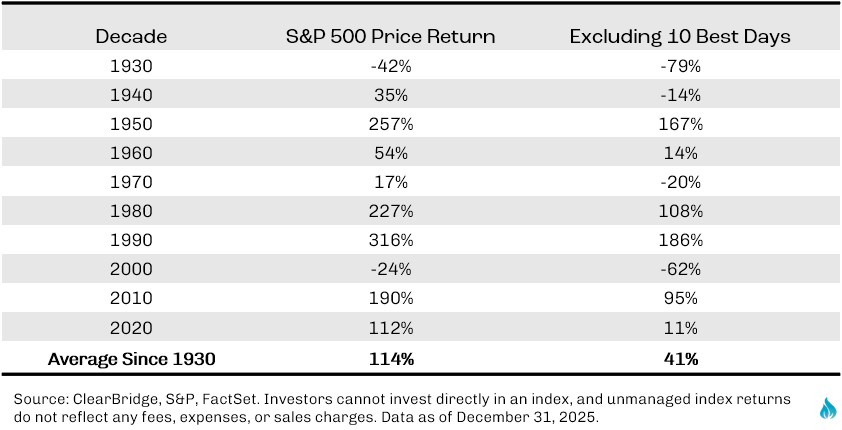

Investor behavior during these periods can have an even greater impact than the events themselves. As shown in the chart below, missing just the ten best days in the market over a decade can reduce total returns significantly.

Importantly, many of the best days in the market tend to occur during periods of heightened uncertainty, often following sharp declines. This creates a challenging environment for investors attempting to time the market, as stepping out during periods of volatility can lead to missing critical recovery periods.

Taken together, these observations reinforce a simple but important principle. While uncertainty can create short-term discomfort, long-term outcomes are often driven more by discipline and consistency than by attempts to react to changing headlines.

These patterns are not just academic observations. They have direct implications for how portfolios should be positioned in an environment where uncertainty is elevated but fundamentals remain intact.

The risks facing markets and the global economy are real, and they are not being underestimated. There are credible scenarios that could challenge both economic stability and asset prices, and we remain focused on them.

At the same time, it is important to remember that we entered the year from a position of strength. The global economy showed resilience, and client portfolios were constructed with a thoughtful balance of growth, diversification, and risk management. That foundation continues to guide our approach today.

There may come a point where conditions warrant a more reactive approach. We understand our responsibility and remain prepared to act if the data and market environment call for it. At this stage, however, we do not believe we are there yet.

Michael is the founder of Fire Capital Management.

.png)