Written by

Kelsey Syvrud, PhD

Written by

Kelsey Syvrud, PhD

Published on

September 11, 2025

Category

Investment Insights

In December 2024, we examined how alternative investments can expand the efficient frontier, enhancing diversification, improving risk-adjusted returns, and tapping into non-traditional sources of alpha. That piece made the case for why alternatives belong alongside public market holdings, particularly in portfolios seeking greater resilience and long-term growth potential.

This article picks up where that discussion left off, shifting the focus from why to how. Over the past few years, private markets have undergone a rapid transformation, driven by regulatory change and new product structures. The conversation has moved beyond institutional investors to include plan sponsors, retirement platforms, and a wider spectrum of wealth clients. Here, we examine some of the forces that are making private markets more accessible and practical considerations for clients across the wealth spectrum who are evaluating this new era of opportunity.

Over the past decade, the barriers separating private markets from the everyday investor have steadily eroded. In just the last 24 months, many of those barriers have fallen away entirely. A wave of changes has opened access points to alternative assets that would have been unimaginable for most retirement savers only a few years ago.

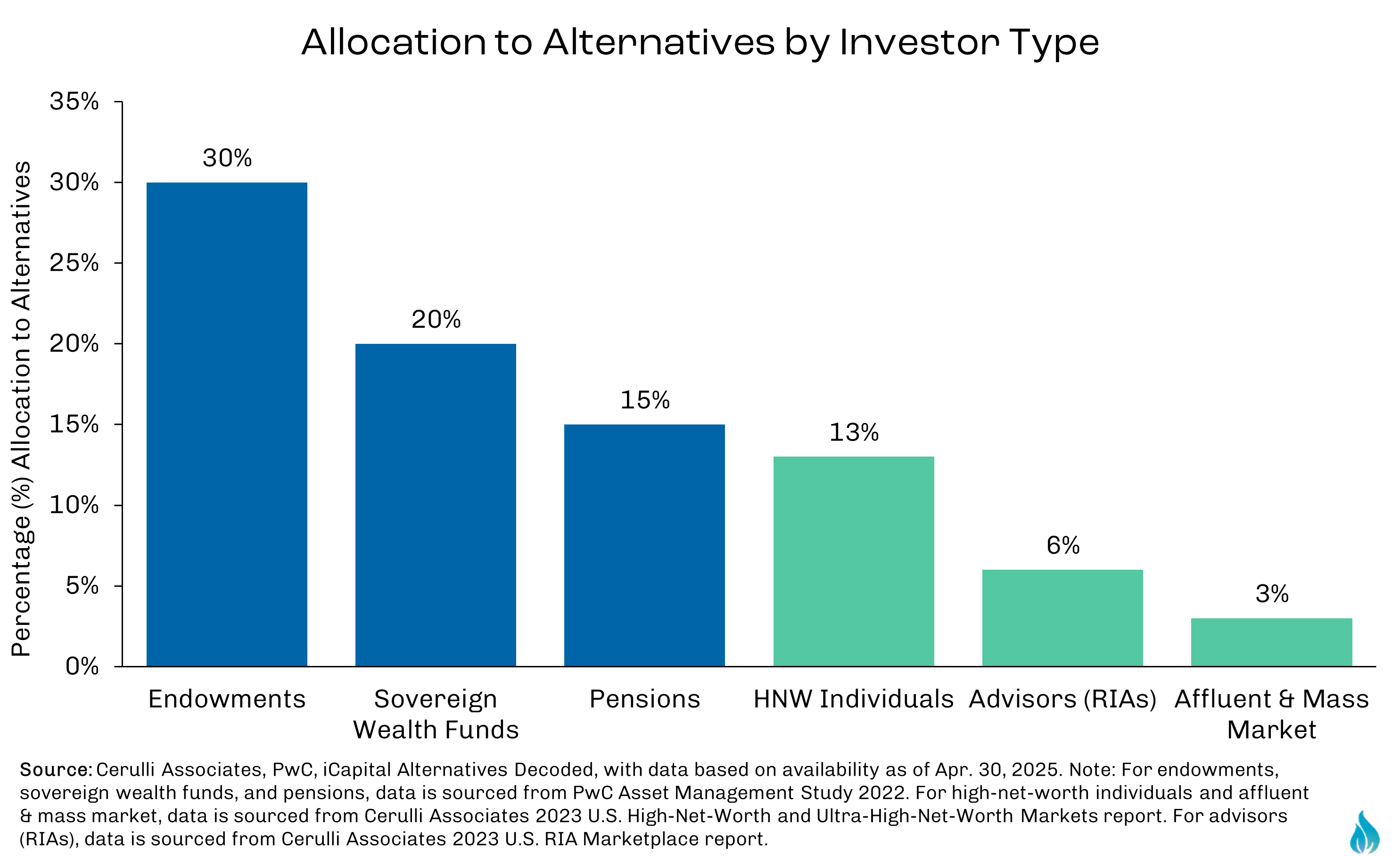

For institutional investors and ultra-high-net-worth (UHNW) families, private markets have long been a core allocation. They have served as engines of diversification, return potential, income generation, and inflation protection. But for mass affluent investors, including many 401(k) participants and IRA holders, these markets remained largely inaccessible. There were clear obstacles including illiquidity, complex capital calls, high investment minimums, and regulatory restrictions designed to shield less-experienced investors from products they might not fully understand.

That reality is changing rapidly. The U.S. Department of Labor (DOL) has clarified how private equity can be incorporated into target-date funds and other diversified retirement plan options. The SEC has shown a willingness to approve semi-liquid structures such as interval funds, tender offer vehicles, and hybrid models that blend public and private assets. Asset managers have introduced “evergreen” formats designed to provide ongoing subscriptions and periodic liquidity, while fintech-enabled fund administration has made onboarding, reporting, and cash-flow management far more seamless.

We are now entering a new era, one in which private markets are no longer just the domain of institutional investors, but a potential component of mainstream portfolio construction. Yet greater accessibility does not eliminate complexity. Liquidity mismatches, valuation opacity, multiple layers of fees, and a steep learning curve remain real considerations for both investors and advisors.

The widening of private market access within retirement portfolios has been anything but sudden. It reflects decades of gradual evolution in U.S. fund regulation, paired with a more

recent surge of product innovation, shifting investor demand, and a willingness from policymakers to revisit long-standing restrictions.

For much of the modern investment era, the Investment Company Act of 1940 (“the ’40 Act”) defined the operating framework for mutual funds and other registered investment companies. These rules were designed with public markets in mind, emphasizing daily liquidity, transparent pricing, and standardized disclosure for the protection of retail investors.

One of the most consequential restrictions for private market access was the 15% illiquid asset limit. This cap was intended to ensure that mutual funds could meet redemption requests promptly, preventing investors from being locked into positions they couldn’t exit in a reasonable timeframe. Under this definition, “illiquid assets” included private equity, private credit, real estate partnerships, and other securities without an active public market.

Even if a manager believed a larger allocation to private markets could enhance portfolio returns, a ’40 Act fund simply could not exceed the cap without violating the rule.

This safeguard was practical in the pre-digital era, when daily NAV calculations and liquidity management were operationally cumbersome. But it also meant that for decades, registered retail products could only offer a token exposure to private markets. The majority of private asset investing remained confined to closed-end, drawdown structures accessible primarily to accredited investors, large institutions, and UHNW families.

The first meaningful shift came in the 1990s with the introduction of interval funds, a registered ’40 Act structure designed to offer periodic, rather than daily, liquidity. This gave managers the

flexibility to allocate more substantially to illiquid holdings while aligning redemption terms with the underlying asset mix. Because interval were not obligated to meet daily redemptions, they could exceed the 15% illiquid asset cap that constrained traditional mutual funds.

At first, adoption was modest. Many advisors and investors were unfamiliar with the mechanics, and operational infrastructure for supporting these vehicles was still developing. But the concept created a regulated pathway for retail-accessible funds to hold a meaningful portion of private market assets.

That early groundwork is what enables today’s reality of a rapidly expanding universe of registered and semi-registered vehicles that effectively bridge the gap between public market liquidity and private market opportunity.

While the concept of periodic liquidity had existed for decades, the real acceleration in private market access came in the past few years. A major catalyst arrived in June 2020, when the U.S. DOL issued an Information Letter clarifying that fiduciaries of defined contribution plans could, under the ERISA “prudent expert” standard, include private equity exposure within diversified, professionally managed options such as target-date funds. This did not open the door to standalone private equity funds inside 401(k) menus, but it gave plan sponsors and asset managers the regulatory green light to begin exploring the possibilities.

At the same time, the U.S. Securities and Exchange Commission (SEC) demonstrated greater flexibility in approving a broader range of semi-liquid structures. This included perpetual-life funds, expanded interval fund designs, and hybrid BDC-style vehicles that combine illiquid, private market assets with a liquidity sleeve of public securities. These innovations allow managers to meet periodic redemption windows without jeopardizing portfolio stability, an important advancement for scaling private market access to a broader investor base.

NASAA and state regulators generally aligned with these changes but continue to stress investor education, disclosure clarity, and suitability. Their focus on transparency, particularly around valuation methodologies and redemption mechanics, has helped ensure that innovation in product design remains grounded in investor protection.

This combination of regulatory clarity and structural flexibility has set the stage for the rapid proliferation of private market vehicles now entering the retail and retirement plan space.

More recently, the conversation around private market access has moved from investment committees to the center stage of industry conferences and major financial media outlets. What was once a specialized allocation for institutional portfolios has become a topic of active exploration for wealth management platforms and financial advisors serving a far broader client base.

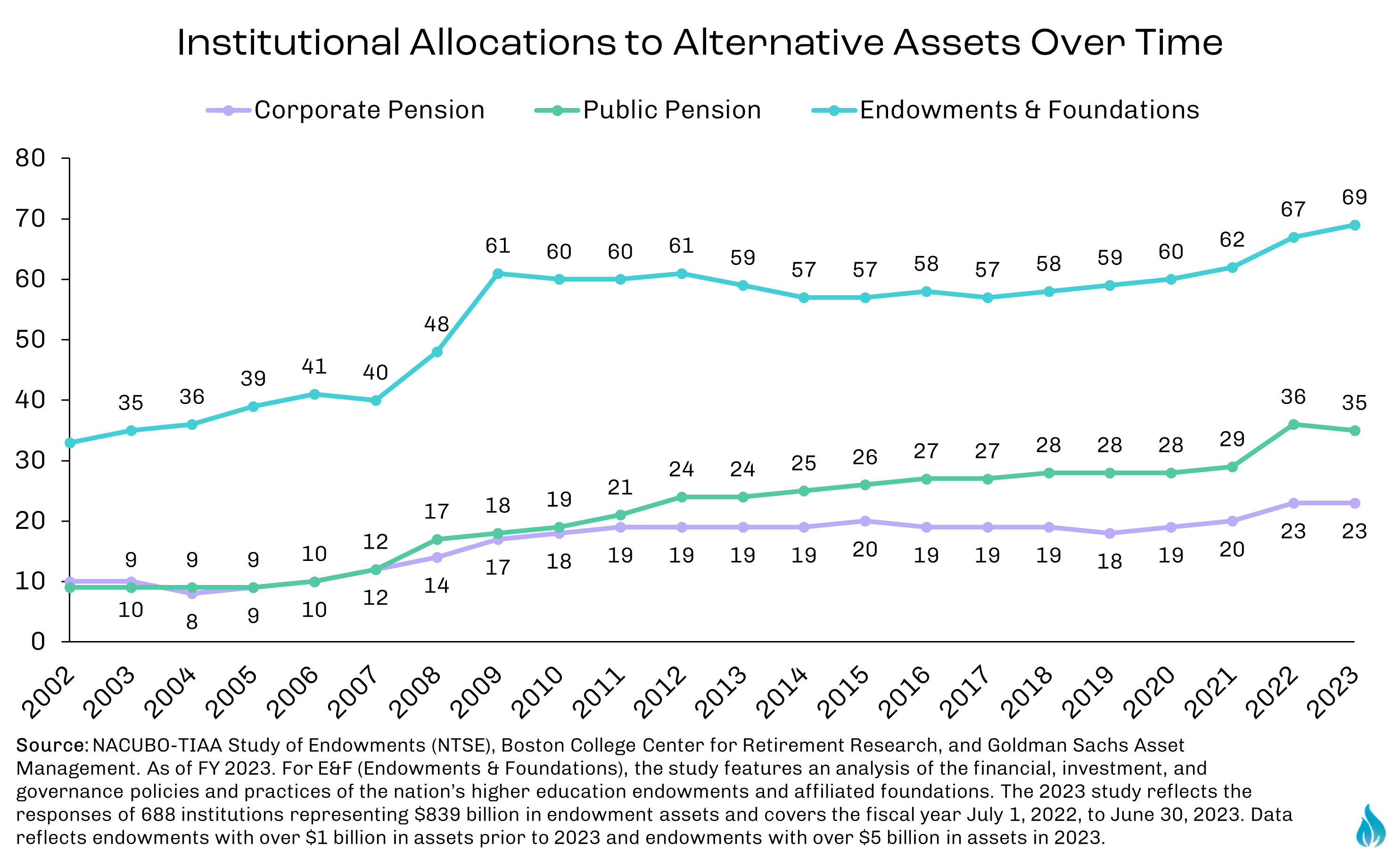

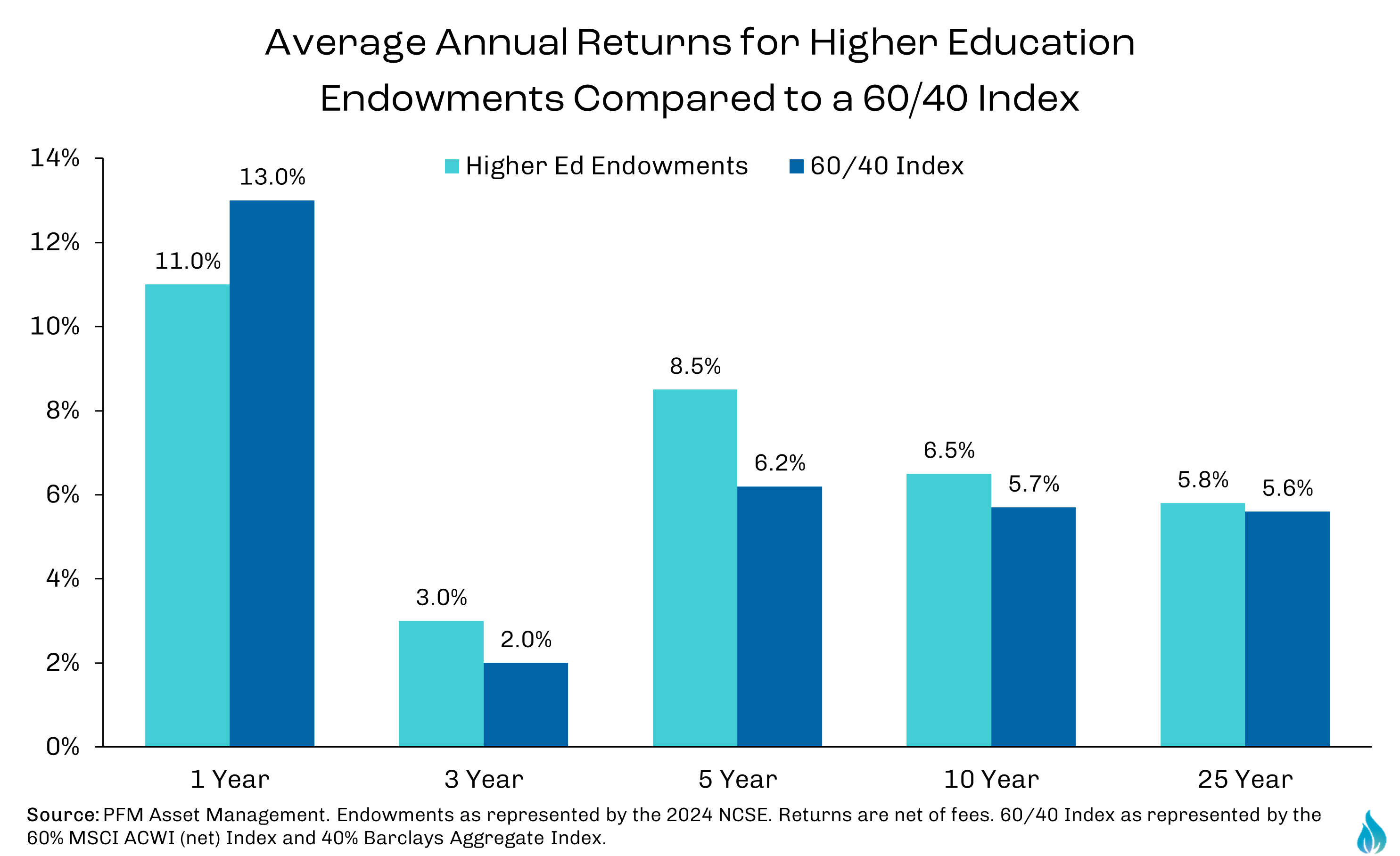

Performance has been an important driver of this shift. While 2024 proved challenging for many private strategies, long-term track records tell a different story. Endowments, foundations, and pension funds with disciplined private market allocations have consistently outperformed traditional 60/40 portfolios over multi-decade horizons. A 2025 University of North Carolina study further confirmed that select private asset classes deliver strong risk-adjusted returns, validating the role of these assets in enhancing long-term portfolio resilience. These institutional results have become a powerful reference point for sponsors and advisors.

Simultaneously, some of the largest alternative asset managers firms, including Blackstone, Apollo, and KKR, have made retail and retirement channels a strategic growth priority. These firms are engineering purpose-built vehicles that balance private market exposure with liquidity, transparency, and compliance features tailored to a wider investor base.

As with many tends, technology is also accelerating this democratization. Platforms such as iCapital, SUBSCRIBE, and CAIS are lowering operational barriers through fully digital onboarding, streamlined KYC/AML compliance, and integrated reporting. These capabilities can allow advisors to efficiently extend private market access to clients with smaller accounts, without sacrificing due diligence or operational rigor.

Finally, the competitive pressures within the retirement plan industry have accelerated the trend. Providers are increasingly incorporating private markets into target-date funds and other default options to differentiate offerings and enhance participant outcomes. For instance, State Street’s new Target Retirement IndexPlus strategy includes a 10% private markets sleeve via Apollo, designed to enhance diversification and return potential. Similarly, BlackRock, with Great Gray Trust, has launched a custom glidepath featuring private equity and credit allocations, projecting an additional 50 basis points (0.50%) annually in returns, which could compound into nearly 15% more in retirement savings over a 40-year term. Goldman Sachs further notes that defined-contribution sponsors are actively evaluating private market integration to improve participants' long-term outcomes.

The result is a fundamental swing in the accessibility conversation. With a host of factors bringing these strategies to a broader range of investors, private markets are becoming a mainstream consideration in portfolio construction, with many shops considering an alternatives allocation table stakes.

For our UHNW and institutional clients, when appropriate and suitable, private markets have been a core allocation in portfolios. These clients are accustomed to committing capital to drawdown structures, carefully pacing commitments across vintage years, managing risks, and building deliberate illiquidity budgets that align with long-term objectives. In these portfolios, alternatives and private market investments are integrated into the broader asset allocation, supported by deep due diligence and disciplined monitoring.

Where recent developments are potentially most transformative for our HNW and emerging wealth clients. For these investors, recent changes present a new opportunity to gain meaningful private market exposure without locking capital for 10+ years. This shift opens the door for smaller taxable portfolios to access institutional-caliber strategies within vehicles designed for their liquidity and operational needs. It also enables more dynamic portfolio construction while maintaining flexibility for rebalancing and cash needs.

But access alone is not a strategy. The democratization of private markets demands careful planning to ensure that allocations align with the investor’s total financial picture. Illiquidity budgets must be right-sized to avoid cash shortfalls during market stress, and cash flow planning must consider periodic redemption schedules, the possibility of redemption gates, and the inherent valuation lags in private assets. At the same time, manager selection takes on heightened importance, as the quality of offerings can vary widely across the expanding product universe.

This democratization of access is noteworthy, but it also raises a challenge: just because you can access private markets doesn’t mean you should, or that every structure fits every investor profile.

At Fire Capital Management, we approach this landscape with the same institutional rigor we apply to large-scale allocations. That means evaluating the structure, the manager’s track record and capabilities, as well as the strategy style, ensuring that each investment fits within a client’s overall portfolio objectives. Our role is to ensure that the increased accessibility of private markets translates into measured, strategic integration, not simply participation in the latest product trend.

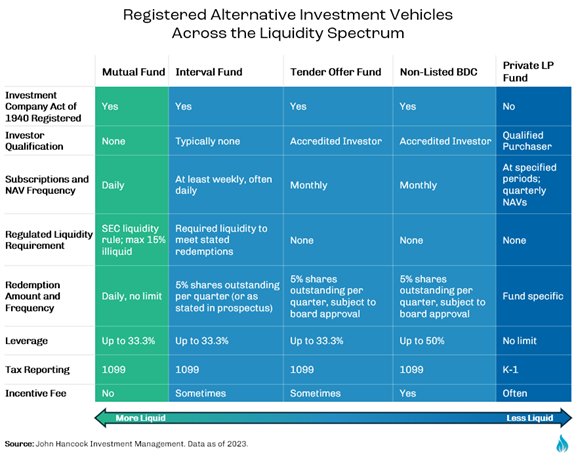

The regulatory tailwinds have opened the door for broader private market participation, but the real point of entry for investors is the structure itself. Each vehicle sits at a different point along the liquidity–return spectrum, with trade-offs in accessibility and potential illiquidity premium. Understanding those trade-offs is important for aligning private market exposure with an investor’s specific needs and circumstances.

For decades, the gold standard for institutional and UHNW investors was the traditional closed-end, drawdown-style fund. These vehicles typically operate over 8 to 12 years, calling committed capital over an investment period and returning it gradually as underlying investments are exited. The drawdown model allows managers to time capital deployment to market opportunities, underwrite deals with “patient capital,” and create value through active ownership. Typically, management fees are charged on committed capital during the investment period, and performance fees are earned only after a preferred return or hurdle is met.

This approach maximizes the potential illiquidity premium but also demands absolute commitment. There are no redemptions, and they often include multi-year lockups. Moreover, it enforces the need for careful liquidity planning to meet capital calls. For UHNW families and institutions, pacing commitments across multiple vintage years can smooth the J-curve and manage risk. For smaller accounts or retirement savers, however, the all-or-nothing liquidity profile makes this structure less practical.

Semi-liquid options bridge the gap between pure illiquidity and fully liquid mutual funds. Tender offer funds, for example, allow redemptions at the manager’s discretion, often quarterly, semi-annually, or annually, through a formal “tender” process. This flexibility enables managers to preserve portfolio integrity while providing periodic liquidity when conditions allow. The trade-off is uncertainty. Investors may not be able to redeem when they want to, particularly during stressed markets. These funds can serve as a tactical liquidity sleeve but should never be counted on for emergency access.

Interval funds move a step further toward liquidity. As registered ’40 Act vehicles, they commit to offering redemptions at pre-set intervals (commonly quarterly) for a stated percentage of shares, often 5–25% of net assets. To honor that liquidity, they hold a mix of private and public assets, using the public portion as a liquidity sleeve. This makes them operationally viable in retirement accounts and potentially attractive for HNW and mass affluent investors who value predictable redemption windows. The trade-off is a somewhat diluted pure-private exposure compared to drawdowns or certain tender funds. For UHNW clients, interval funds often serve as a complement to more illiquid holdings, offering a release valve within the illiquidity budget.

Evergreen funds, also called perpetual-life or semi-liquid funds, have no fixed term, continuously accept subscriptions, reinvest proceeds, and offer periodic redemption opportunities subject to gates or caps. Many of the newest retirement-plan-ready private equity and private credit products fall here. Operationally, they are easier to integrate into defined contribution plans and brokerage platforms because they avoid capital calls and the unpredictability of tender offers. For newer private market investors, retirement savers, or those with lower tolerance for illiquidity, evergreen structures may serve as an entry point. Again, the liquidity sleeve and ongoing capital inflows can dilute exposure to the making them more of a complement than a replacement for traditional drawdown funds in sophisticated portfolios.

At Fire Capital Management, we see these vehicles as tools used to assist in building well-constructed allocations to alternatives and private market products in a diversified portfolio. For UHNW families and institutions, the foundation remains in carefully paced drawdown commitments across vintage years which may be complemented by targeted sleeves in interval or evergreen funds for tactical flexibility. For HNW and mass affluent investors, interval and evergreen funds can be a gateway to private markets, provided allocations are sized appropriately within an overall illiquidity budget.

While structure is important, from a portfolio construction standpoint, retirement integration goes beyond access. It is important to consider the alignment, or misalignment, between the liquidity characteristics of private markets and the liquidity demands of a retirement plan participant base. Getting that balance wrong can undermine both the investor experience and the investment outcome.

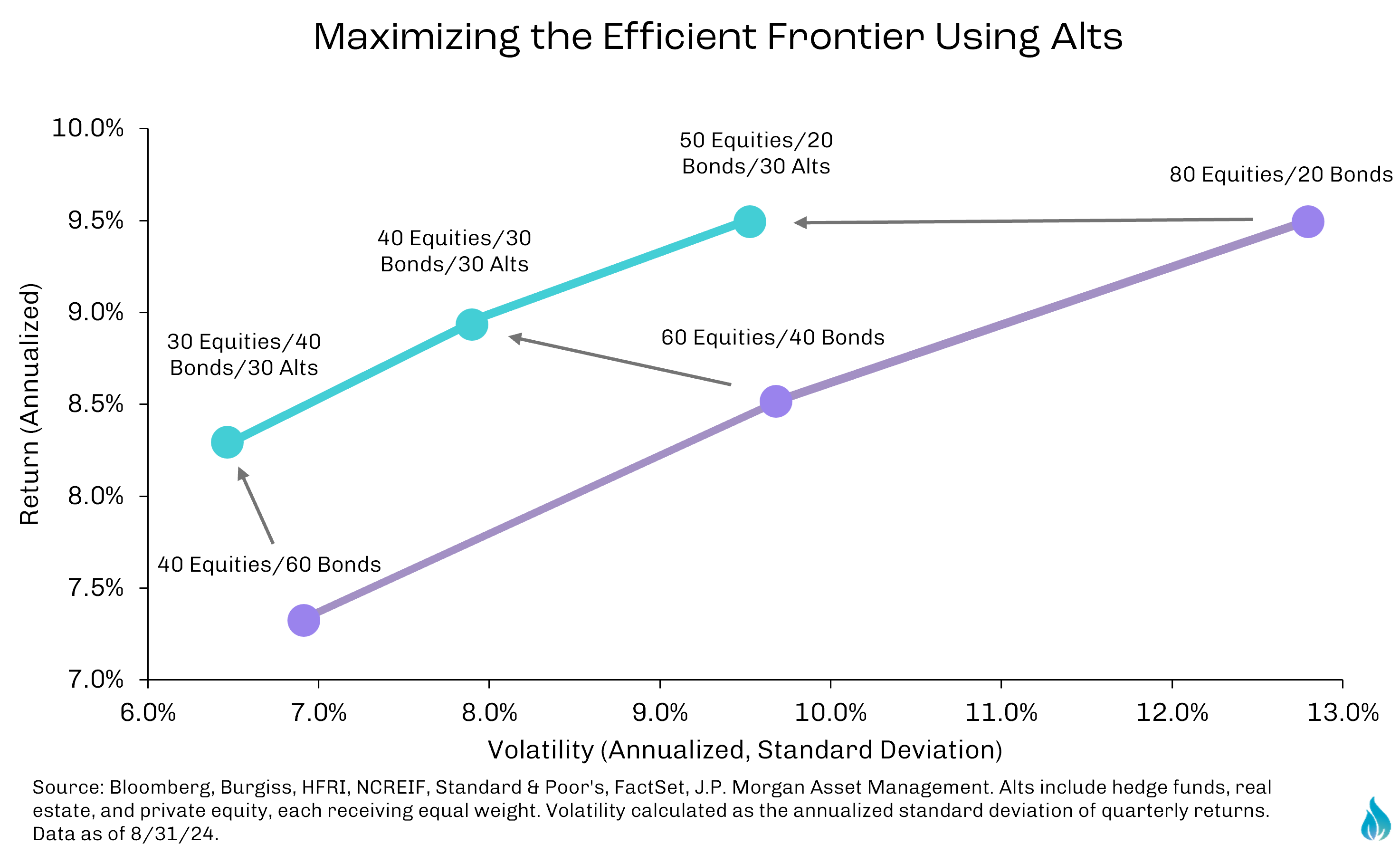

The most immediate and widely discussed benefit of integrating private markets into retirement portfolios is diversification. Public markets, especially in periods of high correlation between equity and fixed income returns, can struggle to deliver consistent risk-adjusted performance. Adding alternative investments to the mix introduces exposure to return drivers that are not always synchronized with public market cycles.

As we discussed in our December article, a second advantage lies in the potential for enhanced long-term returns. While illiquidity is often framed as a disadvantage, it is precisely this characteristic that can allow private market managers to capture a return premium. Without the pressure of daily pricing or the need to manage flows in and out of the fund, managers can take a longer-term, more strategic approach to value creation. For example, this can be done through operational improvements in portfolio companies, patient credit underwriting, or holding real assets through multi-year development cycles.

There is also a behavioral benefit worth noting. Retirement savers who gain exposure to private markets through professionally managed vehicles are less likely to engage in short-term, emotion-driven trading that can erode long-term returns. The inherent lockups or redemption restrictions create a form of “forced discipline,” encouraging investors to stay the course through market volatility, though it may feel uncomfortable at the time.

Against these benefits, there are serious considerations that must be addressed before integrating private markets into retirement plans or smaller accounts. Chief among them is the liquidity mismatch risk. Even semi-liquid structures like interval and evergreen funds depend on a liquidity sleeve to meet redemption requests. In stressed market environments, the value of that sleeve can decline at the same time redemption requests rise, creating strain on the fund’s liquidity profile. If not managed carefully, this can lead to gated redemptions or forced asset sales, damaging both returns and investor confidence.

Valuation transparency is another concern. Private market assets are not priced daily based on live market activity; instead, valuations are based on periodic appraisals, models, and comparable market data. While this can smooth volatility in reported Net Asset Values (NAVs), it can also obscure short-term risks and create the perception of stability where underlying asset values may be shifting. For individuals unfamiliar with these nuances, this can lead to misunderstanding and mismatched expectations.

Fees are also highlighted in many of these discussions. Private market strategies tend to carry higher management fees and more fee-levels than traditional public market funds. This reflects the resource-intensive nature of sourcing deals, performing deep due diligence, negotiating terms, and actively managing portfolio companies or assets over multi-year holding periods. While competition and greater retail penetration have driven some fee compression in recent years, the healine all-in cost of private market vehicles remains meaningfully above that of low-cost index-based public market options.

However, high fees in and of themselves are not inherently problematic. As we always reiterate, what matters is the value delivered net of fees. If a strategy produces excess returns, after all fees and expenses, that justify its risk profile and illiquidity, then the higher cost can be entirely rational. Many of the world’s most successful institutional investors continue to pay premium fees for top-tier managers because they believe (and have historically demonstrated) that the alpha generated more than compensates for the expense.

This moves the fiduciary question from a narrow focus on absolute cost to a broader evaluation of cost reasonableness relative to net benefit. That evaluation requires understanding the fees associated with a strategy and structure, the manager’s historical performance net of fees, assessing whether those results can be repeatable, and ensuring that the investment structure is aligned with the clients objectives. In other words, the focus should not be on finding the cheapest option, but on identifying the managers and strategies most capable of delivering durable, after-fee value to participants.

Finally, there is the educational challenge. Many investors have limited familiarity with concepts like capital calls, distribution waterfalls, or gated redemptions. Without clear communication and ongoing client education, even well-structured products can generate confusion or dissatisfaction.

For UHNW and institutional clients, these risks may already be familiar and are often manageable. For example, illiquidity budgets can be carefully calibrated, and pacing can be controlled. For HNW and mass affluent investors, and especially for retirement plans, the challenge lies in achieving meaningful exposure without creating liquidity stress or complexity that outweighs the benefit.

This is where structure selection becomes highly important. Interval funds and evergreen vehicles offer the liquidity features necessary for retirement integration, but at the cost of some private market purity. Drawdown and tender offer funds provide higher potential illiquidity premiums, but with constraints that may not suit the cash flow needs or regulatory requirements for certain investors. The optimal approach depends on creating tailored allocations that align vehicle structure with investor profile, liquidity tolerance, and portfolio objectives, a process that should be anchored in disciplined illiquidity budgeting and complemented with robust financial planning for long-term pacing.

At Fire Capital Management, we believe it’s not just a question of whether these private market strategies should be included in client portfolio, but how they are selected, structured, and integrated into the broader portfolio.

We are carefully reviewing the product innovation ramping in private market delivery and are mindful of the risks that can emerge when illiquidity is misunderstood or poorly managed. Our role as fiduciaries is to leverage new opportunities for access while ensuring that each client’s private market exposure is calibrated to their liquidity needs, investment objectives, and tolerance for complexity.

We view the democratization of private market access not as a temporary product cycle, but as a durable shift in the investment landscape. This will likely continue to evolve as regulatory frameworks mature, and technology improves the operational infrastructure for these vehicles.

However, broader access does not eliminate the structural challenges of illiquidity, valuation opacity, and the need for disciplined pacing. If anything, the influx of new participants into private markets underscores the importance of thoughtful portfolio integration. We believe this requires those who can balance accessibility with discipline, embracing innovation while staying anchored in sound investment principles. Whether designing allocations for those already familiar with private market exposure or those just getting started, our commitment is the same. We aim to deliver exposure to the right strategies, in the right structures, at the right scale, and with the right oversight to generate sustainable, net-of-fee value over time.

Regulatory evolution and structural innovation have brought private market strategies to the threshold of mainstream portfolios. But the opening of that door is not an invitation to rush through without a plan.

The rise of semi-liquid vehicles and evergreen structures represents an expansion of the portfolio construction toolkit. For some investors, these products may provide a first taste of the benefits that private markets have historically delivered to large institutions. For others, they are a tactical complement to an already robust drawdown program, that may help smooth cash flow and fill strategy gaps.

But accessibility does not eliminate complexity. Illiquidity still requires budgeting. Valuations still require scrutiny. Manager selection still demands deep diligence. And most importantly, integration into the total portfolio must be deliberate. This is the frontier where illiquidity meets accessibility. It is a space of enormous potential, but one that rewards thoughtful navigation over opportunistic chasing.

Private markets will continue to evolve, new structures will emerge, regulations will adapt, and investor familiarity will deepen. But our commitment remains unchanged: to be a disciplined, forward-looking partner, helping our clients participate in this evolution with confidence and purpose.

.png)