Written by

Alyssa Heath, CAP

Written by

Alyssa Heath, CAP

Published on

August 6, 2025

Category

Impact

As we pass the mid-year mark, it’s a natural time to revisit the goals and intentions you may have set at the start of the year. That reflection can extend to your charitable giving. Whether you have already made a few contributions or have been waiting until the end of the year, reviewing your impact goals can help you finish the year with purpose.

In addition to conducting your own mid-year giving audit, the first half of the year has brought several important policy changes, including provisions in “The One Big Beautiful Bill” (OBBB), that may influence your charitable and tax planning strategies for 2025 and beyond. This moment is a good opportunity to be strategic, recenter around your values and causes that matter to you, and to be proactive with your philanthropy.

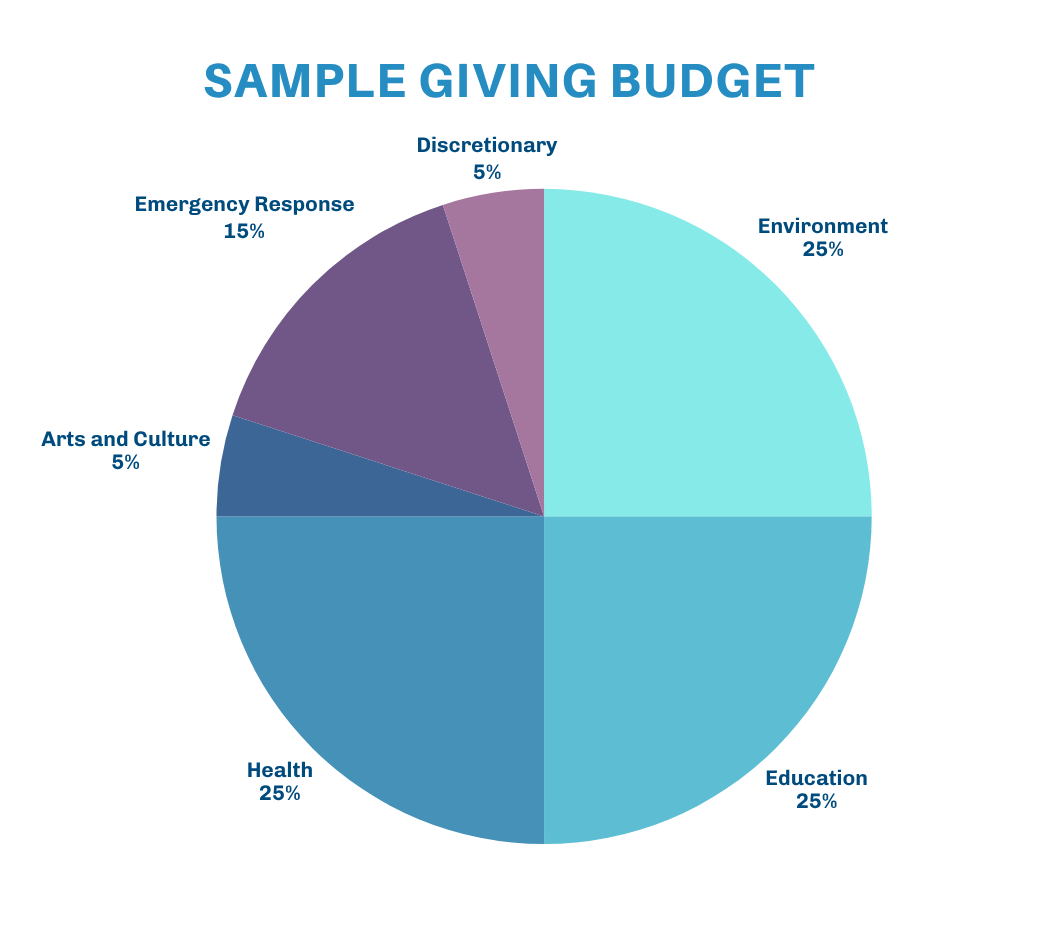

Whether you give through a charitable vehicle such as a donor-advised fund (DAF), a private foundation, or on a more ad hoc basis, a mid-year check-in can help assess where you are in your giving. A few questions to consider:

This is also a good chance to step back and ask: What kind of difference do I want to make this year?

In the last month, you likely have read all about the myriad of policy changes that “The One Big Beautiful Bill Act” (OBBB) enacted. Several provisions in the sweeping tax package have implications for charitable giving:

While several proposed reforms affecting foundations and DAFs did not make it into the final bill, new regulations around distribution requirements and payout timelines are still under consideration. We will continue to watch these closely and report on important outcomes.

While charitable giving is most often driven by values and the desire to make a difference in a particular area, there are also strategic considerations that may help to maximize your impact this year.

This year, many nonprofit organizations are facing funding constraints, making your support more important than ever. Individual giving still comprises about two-thirds of all charitable giving in the U.S. and continues to play a critical role in supporting the causes that impact our communities.

There are ways you can help support your favorite nonprofit organizations beyond just the check. Even if you do not increase your giving, to help nonprofits with their cash flow and planning consider giving the donations earlier, rather than the year-end rush. Additionally, offering unrestricted/general operating support, rather than limiting the purpose of the funds, provides flexibility and allows nonprofits to use funds where it is needed most. You may also try asking your favorite organizations what is most helpful right now. Beyond financial contributions, your time, voice and connections can also make a big difference.

While you don’t need to overhaul your giving plans for the year amidst many economic, social and regulatory changes, it is an opportunity to purposefully re-align your plans to maximize the impact of your giving. Fire Capital supports our clients with their philanthropic strategy, planning, and research on charitable organizations that align with what our client’s care about most. Of course, everyone’s circumstances will affect what strategies make the most sense to them, so it is important to engage with a tax professional or your financial advisor to align with your values and goals so you can give with confidence.

https://cof.org/page/one-big-beautiful-bill-impact-philanthropy

https://ssir.org/articles/entry/eight_myths_of_us_philanthropy

.png)